Investment fees can make a big dent in your portfolio value.

Expense ratio, one potential component of investment fees, is the percentage of a fund’s assets that go toward covering expenses of the fund (e.g. custodial costs or management salaries).

For example:

Fund 1 – 0.5% expense ratio

Fund 2 – 0.1% expense ratio

A rough estimate of the cumulative impact of an annual expense ratio over time is:

where f = expense ratio, n = years

So, if you invest in Fund 1 for 30 years with a 0.5% expense ratio, you will lose ~14% of your portfolio in fees, calculated as 1 – (1 – 0.005)³⁰.

If you invest in Fund 2 for 30 years with a 0.1% expense ratio, you will lose ~3% of your portfolio in fees. The 11% portfolio difference is significant!

As a practical example, there are 2 different S&P 500 funds.

VOO – a Vanguard S&P 500 Index Fund ETF;

SPY – a SPDR S&P 500 ETF Trust.

VOO has a 0.03% expense ratio, while SPY has a 0.09% expense ratio. Over 30 years, that’s almost a 2% portfolio difference. Small percentage differences compound over time.

Expense ratios aren’t unique to ETFs. Mutual funds also charge expense ratios, and the difference can be even larger.

For example, many actively managed mutual funds charge 0.50%-1.50% annually, while broad market index funds often charge less than 0.10%.

Over decades, that fee difference can significantly reduce your ending portfolio value.

Where can you find the expense ratio?

- You can Google it; or

- Summary Prospectus

I prefer Summary Prospectus as it shows all the fees in a detailed view.

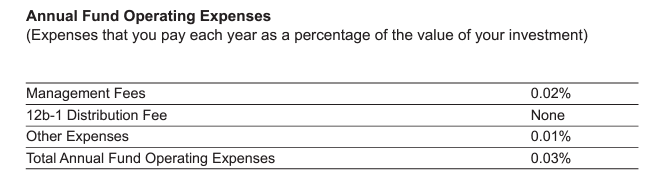

For example, let’s take the Summary Prospectus of VTI, a US total market index fund ETF, which has a 0.03% expense ratio:

The management fee is the money used to pay the manager of a particular fund.

12b-1 distribution fees cover marketing and broker expenses.

Other expenses include the costs of record keeping, mailings, or maintaining a customer service line.

In addition, you want the fund to have a low turnover ratio. A higher portfolio turnover rate may indicate higher transaction costs and could result in increased taxes when the fund shares are held in a taxable account (e.g., through capital gains distributions).

For VTI, the fund has a 2% turnover ratio (buying and selling stocks) and 0% capital gains distribution, making it an extremely tax-favorable investment.

If a fund has a high turnover ratio and distributes capital gains, you will have to pay more in taxes every year if you hold in a brokerage account.

The biggest impact of the expense ratio is within the 401k/403b investment options:

401k/403b

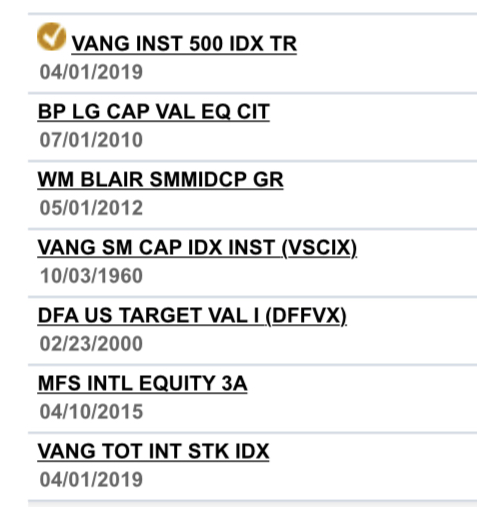

If you are contributing to retirement accounts, you will be able to select different funds.

Now there will be many BAD funds available to you.

Here is a list of some of the funds available to me:

For example, MFS INTL equity has an expense ratio of 0.64%.

Now, the expense ratio isn’t the only thing to look for, but it’s a necessary component to analyze. Oftentimes, you can find funds that track the exact same things (e.g. the S&P 500 index) but have extremely different fees.

Many 401(k) and 403(b) plans primarily offer mutual funds instead of ETFs. This makes expense ratios especially important because some actively managed mutual funds charge 0.50%-1.00% or more per year, while comparable index funds may charge less than 0.10%.

Usually, Vanguard has the lowest expense ratio in the market.

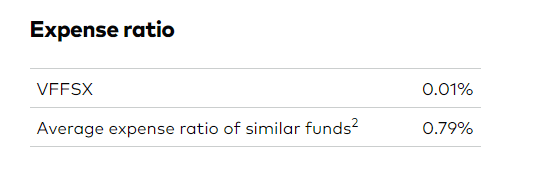

For example, my 401k is invested in the Vanguard Inst 500 Index Trust. (ticker VFFSX)

Look at that expense ratio:

And performance:

I suggest writing down a list of available funds and checking their expense ratios and performance.

Many times, people just select one and never look back at it.

Actionable tip: Open your 401k and look through the investment options. It will save you a lot of money in the long term

I know this is not the most fun topic, but it’s an important one.

See you next Saturday

MC, CPA