On July 4th 2026, Trump accounts (530A) went live. My goal with this newsletter is to tell you everything you need to know about this account, how to open one, rules, and whether it’s worth it from a financial, not political, lens.

Trump account is a new IRA style savings account for kids. Per the IRS, nearly 6 million elections to open a Trump Account had already been filed as of June 2026.

If you’ve got kids, or you’re a grandparent, aunt or uncle who wants to help one, here are all the details you need to know:

Details

A Trump Account is a new type of IRA opened on behalf of a child under 18. Parents, grandparents, other relatives, friends, and even employers can contribute, and the money is invested only in a low-cost U.S. stock market index fund.

There is a lot of confusion about this account because of 2 main things:

- Who can have an account

- Who gets the free $1,000

To open an account, the child must be under 18, and have a valid SSN that’s valid for employment. A parent, legal guardian, or grandparent can serve as the “authorized individual” who makes the election on the child’s behalf to open it.

To get the $1,000 seed deposit, the child must also:

- Be a U.S. citizen

- Be born between Jan 1, 2025 and Dec 31, 2028

- Have the $1,000 election requested (more on this in a bit)

Open it

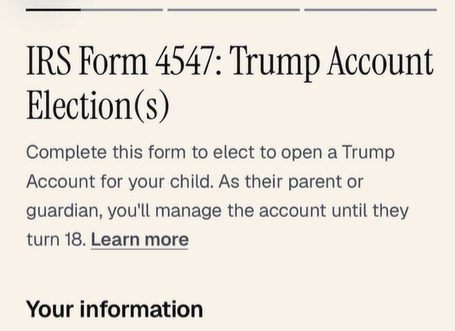

The easiest way to do everything you need (including filing form 4547) is to download the Trump account app on your phone.

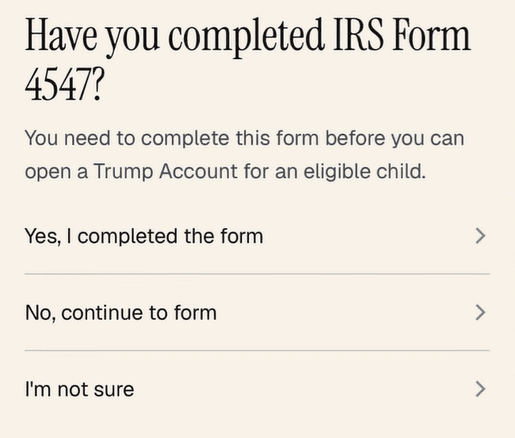

From there, create an account by providing an email & password. Then, you’ll have to verify YOUR name and SSN (not your child’s). The next step asks whether you submitted IRS Form 4547.

If you have filed this form as part of doing your 2025 taxes, select Yes (or if you submitted it on the IRS online account). If you haven’t, then select “continue to form”.

This form will ask for YOUR information, your child’s information, and whether you want to receive the $1,000 seed money (it will let you know if you don’t qualify, fyi)

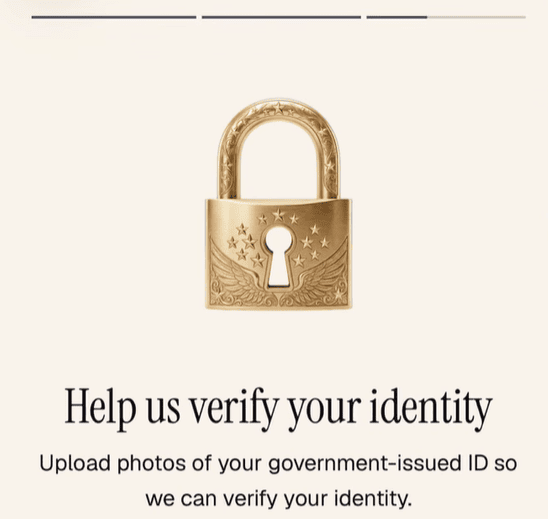

You will also need to verify your government issued ID:

It will take roughly 4-6 hours (ish) to get this form processed, and then you can finish the account setup.

If you already filed the form 4547 as part of your taxes, the setup will be much quicker (just select “Yes, I completed the form” during that prior selection screen)

After the form is processed, you will need to come back and “Finish account setup”. During the final step, it will say something like “Congrats, you child is eligible for the account”, and you will have to verify child’s info again. Once activated and verified, you will be able to make contributions or share the link for other family members to contribute.

Quick $250 check

I know some of you might say “oh my child doesn’t qualify for the $1k”, but let me share about a potential $250 they may qualify.

Dell pledged a significant amount to Trump accounts. To qualify, your child must be age 10 or younger, live in a ZIP code with a median household income of $150,000 or less, and not qualify for the federal $1,000 Treasury seed deposit.

Check this link to see if your child/area qualifies for the $250.

Now, let’s cover a bit more on the account:

Limits

Total outside contributions (from parents, grandparents, friends, and employers combined) are capped at $5k/year. Employers can contribute up to $2,500 per year toward an employee’s child’s account, tax-free to the employee. The $1k deposit, or money from a 501(c)(3) charities, are not subject to the limit.

Investment options

You can’t pick individual stocks. They can only be invested in mutual funds or ETFs with less than 0.1% in expense ratio. The Treasury Department made State Street SPDR Portfolio S&P 500 ETF (SPYM) as the default fund at launch.

Taxes

Contributions from parents, relatives, friends are after-tax (no deduction). The money grows tax-deferred. No withdrawals (unless due to rollover or death) is allowed during the “growth period” (until turning 18).

Starting January 1 of the year the child turns 18, the account becomes a traditional IRA. At that point, you can invest in anything you want (within the IRA options). You can also withdraw it (withdrawals will be taxable and can trigger 10% early withdrawal penalty, unless an exception applies, like $10,000 for a first time home purchase or qualified higher education expenses)

One planning opportunity is that at 18 you could do a Roth conversion (will come with a tax bill), but can have decades of future tax-free growth.

Gift tax

One part that most mainstream media didn’t cover is whether contributions to Trump accounts are subject to gift taxes. The Treasury and the IRS addressed this with Rev Proc 2026-25 creating a safe harbor. If you are an individual (not a trust), only taxable gift that year are cash contributions to one or more Trump accounts, total gifts to that particular child for the year (Trump contributions plus any other gifts) don’t exceed $19,000 for 2026, and you aren’t otherwise required to file a Form 709 (Gift form) for that year, your Trump account contributions don’t need a Form 709 filed.

TLDR: for most people, you likely shouldn’t need to file the Gift form. For sophisticated donors, and wealthy families, it’s something to keep in mind.

Is it the right move?

Here’s how I think about where Trump account fits:

- Get the $1k seed money (if eligible)

- If you want your kids to go to college, do a 529 plan instead

- If you’ve already built up a sizable 529 plan, and your kids have earned income, consider a Roth IRA for them

- Then, if you have the means, you can do a combination of UTMA/UGMA and brokerage account (but make sure your retirement is set too instead)

I hope you enjoyed this one! Let me know if you have any questions.

Chat next week!