Section 415(d) of the IRC requires the Secretary of the Treasury (IRS) to annually adjust limitations for cost-of-living increases. So, let’s dive into some of the changes:

401(k), 403(b), and Most 457 Plans:

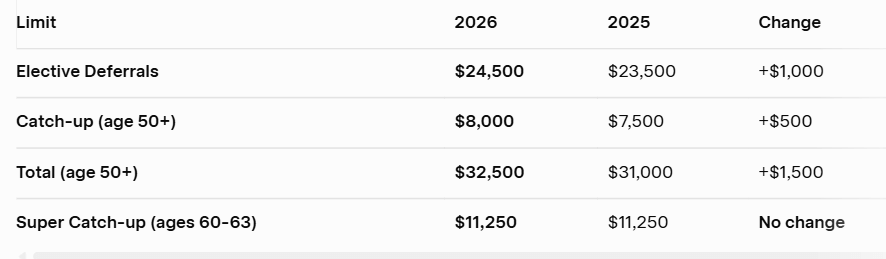

For 2026, the 401(k)/403(b)/457(b) amount you can contribute is increasing from $23,500 to $24,500. If you are in a 24% marginal tax rate, that’s an additional $240 of federal taxes you can defer. If you are over age 50, the catch-up contributions are also increasing by $500, which is a small increase.

Defined Contribution Plans, §415(c)

The annual total contribution limit is increasing to $72,000 (up from $70,000).

This means that your employee contributions + employer contributions + after-tax contributions cannot exceed $72,000 in 2026.

Many people only have employee + employer contributions, but if you are self-employed with a Solo 401(k) or working for a big Fortune 500 tech company, you may have the option of making after-tax contributions. The strategy is called the “Mega Backdoor Roth,” which allows you to contribute thousands extra into your Roth 401(k)/Roth IRA.

IRAs (Traditional & Roth)

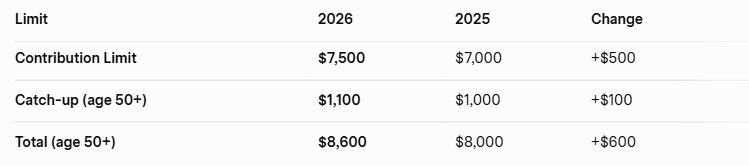

For 2026, the Roth/Traditional IRA limits are increasing by $500 to $7,500.

Note that the Roth IRA income limits to contribute are also increasing in 2026. Direct Roth IRA contributions aren’t allowed if your modified adjusted gross income is over $168,000 (single) or $252,000 (married filing jointly).

However, you can still use the “Backdoor Roth” strategy to get around these income limits by doing a non-deductible IRA contribution that gets converted into a Roth. Just make sure you are aware of the pro-rata rule.

Other Adjustments

Earlier in the month, IRS released more details on other key adjustments for 2026:

1. Standard deduction

Married filing jointly: $32,200 (from $31,500)

Single: $16,100 (from $15,750)

Heads of households: $24,150

Note that the OBBBA also increased the standard deduction from $15,000 to $15,750 for 2025.

2. Estate tax exclusion

The estate tax exclusion is increasing from $13,990,000 in 2025 to $15,000,000 in 2026 due to OBBBA changes.

3. HSA

In 2026, you can contribute up to $4,400 if you are covered by a high-deductible health plan just for yourself, or $8,750 if you have coverage for your family to HSA.

4. Tax Brackets

All tax bracket limits are increasing by ~4%. Here are the 2026 brackets:

- 12% for incomes over $12,400 (over $24,800 for married couples filing jointly)

- 22% for incomes over $50,400 (over $100,800 for married couples filing jointly)

- 24% for incomes over $105,700 (over $211,400 for married couples filing jointly)

- 32% for incomes over $201,775 (over $403,550 for married couples filing jointly)

- 35% for incomes over $256,225 (over $512,450 for married couples filing jointly)

- 37% for incomes over $640,600 (over $768,700 for married couples)

5. QCD

The QCD limit (age 70½+) is also increasing to $111,000 (from $108,000), which is the maximum charitable gift from an IRA that can be excluded from your income.

So overall, most of the deductions or limits are increasing by 3–4% on average.

Take advantage of these limits and maximize your tax-efficient retirement savings!

Chat next week!

MC, CPA