Learning about different asset protection strategies is just as important as building wealth.

Quick disclaimer: I’m not a lawyer, and this is just my personal interpretation of various federal laws. Please contact a lawyer if you need specific advice.

401(k)/403(b) Plan

Investing in a 401(k) or 403(b) plan is a good way to protect your assets.

The Employee Retirement Income Security Act (ERISA) protects retirement plans from creditor judgements. It also protects against bankruptcy, and applies in all U.S. states.

Most 403(b) plans are also covered under ERISA, though some exceptions apply (e.g., religious organizations). Maximizing contributions to a 401(k) or 403(b) is a great strategy for not just building wealth but also protecting your assets.

Rollover IRA

If you quit your job and roll your 401(k) into a rollover IRA, what happens to your asset protection?

Based on my research, if you roll your 401(k) or 403(b) into an IRA, it’s protected in federal bankruptcy, with no limit on the amount.

Outside of bankruptcy, asset protection against creditors (e.g., during a lawsuit) is governed by state laws. Some states offer unlimited asset protection, while others cap it at certain amounts (more on this in a bit).

If you have both a rollover IRA and a 401(k) plan, it’s generally recommended to roll that IRA back into your 401(k) to obtain the best asset protection. However, if your 401(k) plan doesn’t offer good funds with a low expense ratio, that’s something to consider. Rolling a rollover IRA into a 401(k) can also be beneficial if you plan to use the Backdoor Roth strategy.

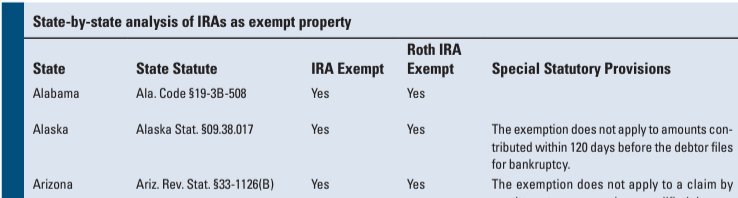

Traditional IRA/Roth IRA

For situations other than bankruptcy, protection of Traditional IRAs and Roth IRAs from judgments is determined by state law.

Be sure to check your specific state’s laws to understand the level of asset protection available:

At the federal level, the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 provides an exemption for traditional IRAs and Roth IRAs up to $1 million, adjusted for inflation (~$1.5 million in 2024).

It’s important to differentiate between traditional IRA/Roth accounts where you contributed versus rolling amounts from a traditional/Roth 401(k) into a rollover account, as different rules apply (e.g., separate accounts for rollovers versus contributions).

In general, retirement plans can be tapped for family support, divorce, or through federal tax liens.

Primary Residence

Many states offer a ‘homestead exemption,’ which means that some or all of your principal residence’s equity is protected from creditors. However, this varies by state.

Arkansas, Florida, Iowa, Kansas, Oklahoma, South Dakota, and Texas offer unlimited homestead exemptions, allowing you to protect significant wealth by purchasing more expensive homes.

Other states, like California, have exemptions ranging between $300,000 and $600,000, depending on the median home sale price in the county. In Illinois, for example, the homestead exemption is only $15,000 (doubled for married individuals).

Insurance

Insurance is also a good asset protection strategy. Specifically, umbrella insurance can provide security beyond your other insurance policies (such as auto or landlord insurance).

Complex strategies

There are a few other strategies, but they are outside the scope of this newsletter.

- LLCs – If you own a business that carries a high risk of liability, forming an LLC can be a good way to protect your assets. However, be mindful of the risk of “piercing of corporate veil”

- Irrevocable trusts – type of trust that generally cannot be changed once established. Whatever you contribute to the trust belongs to the trust, not to you. Your family can then be the beneficiary of that trust.

- Off-shore trusts