We’ve always heard that withdrawing your 401k or IRA before 59½ would come with a penalty.

Well, I’m here to tell you that there is a loophole that allows you to withdraw much earlier. You can withdraw at 40, 50, or any age!

In the IRS tax code, there is a section called 72(t)(2)(A)(iv) that states an exception to the 10% penalty if you can establish a “series of substantially equal periodic payments over the life expectancy.”

To calculate the amounts you can withdraw from your 401k or IRA, we need to determine the following:

- The applicable interest rate

- Life expectancy

- Method

- Account balance

1. Interest rate

The interest is the greater of:

- 5%; or

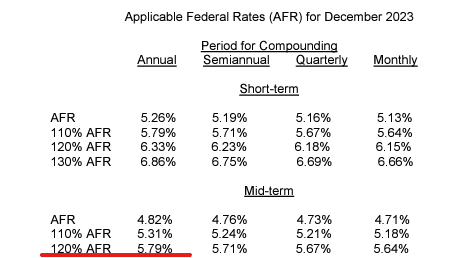

- 120% of the federal mid-term rate published in IRS Revenue Rulings (applicable federal rates) for either of the two months immediately preceding the month in which the first payment of the SoSEPP is made.

If you want to start withdrawing in February, your interest rate will be the highest of the following options: 120% of the federal mid-term rate for January, 120% of the federal mid-term rate for December, or 5%.

From these tables, we can see that the highest interest rate is 5.79%.

2. Life expectancy

The life expectancy is calculated by a few different methods:

- Uniform Lifetime Table in Appendix A of Notice 2022-6,

- Single Life Table in Section 1.401(a)(9)-9(b),

- Joint and Last Survivor Table in Section 1.401(a)(9)-9(d).

But, the single life table usually results in the highest withdrawal amount.

3. Method

The IRS defines 3 methods to establish these equal period payments:

A Minimum Distribution Method (variable withdrawals)

Amortization Method (static withdrawals)

Annuity Method (static withdrawals)

I suggest using Amortization or Annuity, as they are static and require no recalculations every year.

4. The account balance

You can determine the portion of your account subject to distribution. No contributions or withdrawals (except those outlined in the plan) can be made from the designated account. If you want to use only a portion of your IRA, you can roll that specific amount into another IRA.

Importantly, the rule must be maintained for a minimum of 5 years or until age 59.5, whichever is later. For example, if you establish it at 50, you will need to continue withdrawing until 59.5. Failure to maintain withdrawal will result in the retroactive 10% penalty for all years

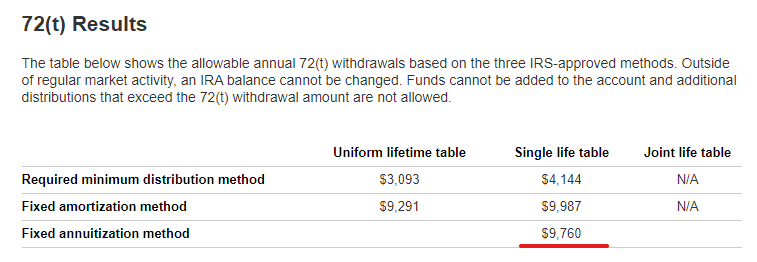

Here is how it works:

Say you have $200,000 in your IRA (you can roll 401k into an IRA once you are ready to retire), and transfer $150,000 of it to the other IRA to be subject to 72t rules.

With these assumptions:

Interest rate: 5.79%

Account balance: $150,000

Your Age: 50 y.o

The results from using a calculator:

So, you can start withdrawing $9,760/year (schedule these withdrawals every year) and will have to do so until you get to 59.5.

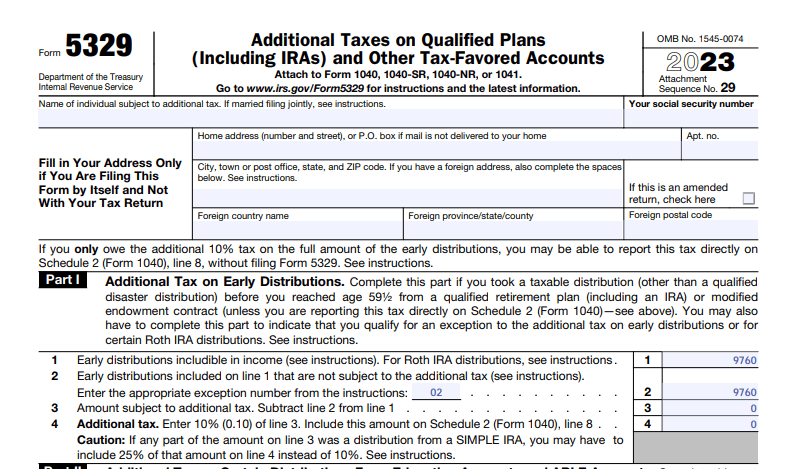

From the tax form standpoint, you will need to file a form 5329, “Additional taxes on qualified plans”.

On line 1 and 2, you need to enter the amount you withdrew, and the exception number is 02.

While this may seem all complicated, it’s actually pretty easy to determine.

This allows access to your retirement funds a lot earlier.

I hope you enjoyed this and & share this email with friends!

See you next Saturday.