If you receive a windfall, a bonus, or maybe you were saving for something but plans changed, how would you invest the cash?

Would you invest it all at once (lump sum), or would you invest a portion every month or week (dollar cost averaging)?

I analyzed Vanguard’s research titled “Cost Averaging: Invest Now or Temporarily Hold Your Cash” to help answer these questions.

Let’s run through an example.

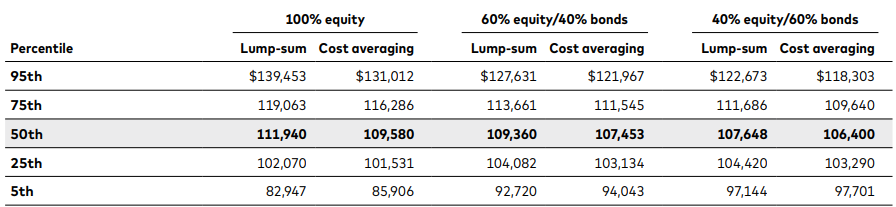

Say you have $100,000. You can invest it all at once or split it into three equal parts and invest each part one month apart. What would the value be in exactly one year?

Vanguard ran this calculation using the Total Market Index for the years 1976 to 2022. They found that, regardless of the portfolio allocation, lump sum investing outperformed cost averaging most of the time:

You can also run a similar projection using portfolio backtesting websites.

For example, if you invested $10,000 in VTI on January 1, 2021, by December, you would’ve had $12,567:

What if you instead invested $833 for 12 months? You would have $11,477, or about $1,090 lower.

This is simply because the $10,000 you invested had 12 months to grow, and 2021 was a favorable market where VTI experienced 25% growth.

This brings up an important point: cost averaging hinders portfolio growth in rising markets; however, it provides protection in downturns.

To illustrate this, say you invested $10,000 in February 2020. In just one month, it would have fallen to $7,000 due to pandemic drop. Obviously, it recovered later on, but cost averaging would have protected you from this significant downside.

Now, unfortunately, we don’t know what will happen in 2 weeks, 6 months or 2 years with the stock market. This is why we have to rely on the data.

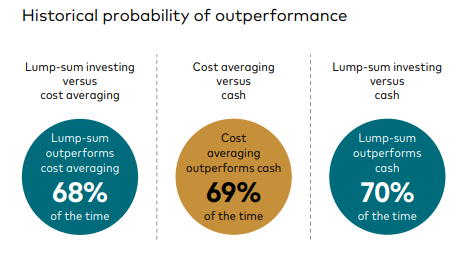

According to Vanguard’s research, lump sum investing outperforms cost averaging 68% of the time:

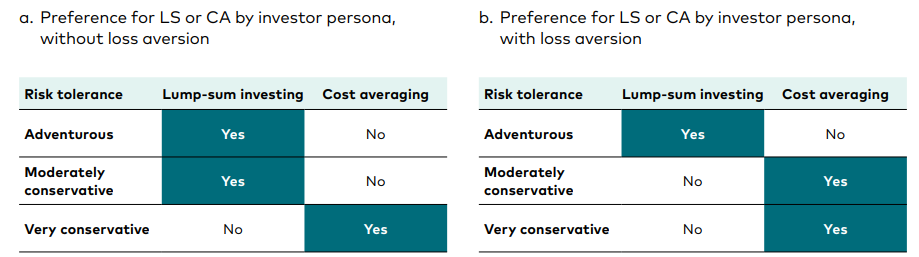

The numbers are clear. But what if you want to avoid big losses and are okay with sacrificing some growth (typically described as being “loss-averse”)? In this case, behavioral factors need to be included in the calculation.

Based on Vanguard’s model, you should consider sticking to cost averaging if you have a very conservative investor persona.

How else could you apply the findings?

Most of us won’t win the lottery or inherit a substantial amount. One practical application is to “front-load” your 401(k). If possible, an investor could significantly increase their 401(k) contributions until the account is maxed out early in the year. But you also need to consider any matching contributions you receive, as some companies don’t match if you don’t contribute.

My final thought

Ultimately, regardless of whether you choose dollar-cost averaging or lump sum investing, one thing is clear: you have to invest.

Having a plan for investing cash is the most important part. Choosing one strategy over the other will only make a marginal difference compared to keeping cash long-term.

I hope you enjoyed this one and learn something new. Any feedback? You can always reply to this email.

See you next Saturday.