I know some people who don’t contribute to a 401(k), IRA, or 403(b) because they want to retire early. They don’t want to wait until 59 ½ to pull the money out without the 10% penalty. Or perhaps some are worried about being forced to retire early and accessing that money.

Well, I’m here to tell you that your retirement plans can actually be a lot more flexible than you think.

And you can withdraw at 40, 50, or any age, as long as you follow the rules. Now, I’m not recommending you withdraw early from it, unless for early retirement purposes, but it’s good to be aware of this rule.

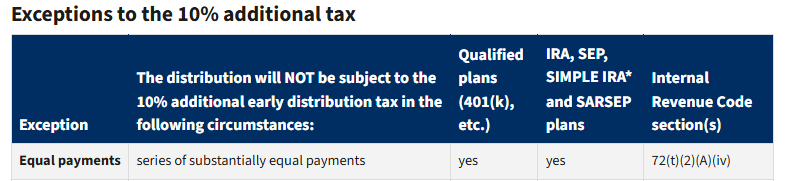

In the tax code, there is a section called 72(t)(2)(A)(iv), also commonly referred to as 72(t) or SoSEPP, that outlines an exception to the 10% penalty if you can establish a “series of substantially equal periodic payments” over your life expectancy:

In simple terms, this means that the IRS allows you to withdraw a specific amount based on your balance and life expectancy without the 10% penalty.

Background info

Once you establish this withdrawal plan, no contributions or withdrawals (except those outlined in the plan) can be made from the designated account.

Importantly, the plan must be maintained for a minimum of 5 years (plus one extra day for safety) or until age 59½, whichever is later. The plan would start on the date of the first SoSEPP distribution.

For example, if you establish the withdrawal plan at age 50, you will need to continue withdrawing until 59½. Failure to maintain the withdrawals will result in a retroactive 10% penalty for all prior years. However, some Private Letter Rulings (PLR 201051025 and PLR 200503036) have previously provided relief due to a custodian error.

Rev. Rul. 2002-62 also allows you to make a one-time change to the required minimum distribution method, which usually results in lower payouts (useful in bear markets, etc) if use the amortization or annuitization method (more on this in a bit).

How do we calculate the amounts we can pull without penalty?

To calculate the amounts you can withdraw from your 401k or IRA annually without the 10% penalty, we need to determine the following:

- Interest rate

- Life expectancy method

- Withdrawal method

- Balance

P.s. I will also have an example in a bit

> Interest rate

You must choose an interest rate that does not exceed the higher of the following two rates:

- 5% or

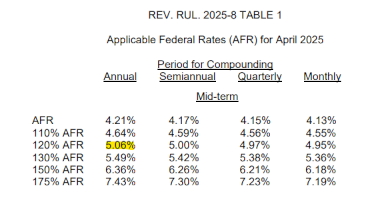

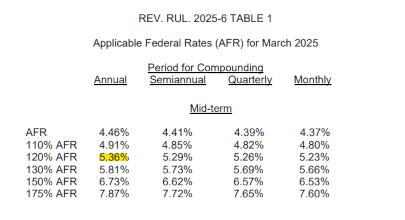

- 120% of the federal mid-term rate published in IRS Revenue Rulings (applicable federal rates) for either of the two months preceding the month in which the first payment of the SoSEPP is made.

Generally, the higher the interest rate, the higher the calculated amounts. We can use either the April or March table, for which the annual federal mid-term rates are 5.06% and 5.36%, respectively.

The interest rate depends on the frequency of these payments (i.e, the compounding period) you want to withdraw.

Let’s stick with annual withdrawals for simplicity. Since we can choose the higher of the two, let’s go with 5.36% as our interest rate.

> Life expectancy

The life expectancy is calculated:

Uniform Lifetime Table in Notice 89-25

Single Life Table in Section 1.401(a)(9)-9(b)

Joint and Last Survivor Table in Section 1.401(a)(9)-9(d)

The single life table usually results in the highest withdrawal amount.

> Method

The IRS defines 3 methods to establish these equal period payments:

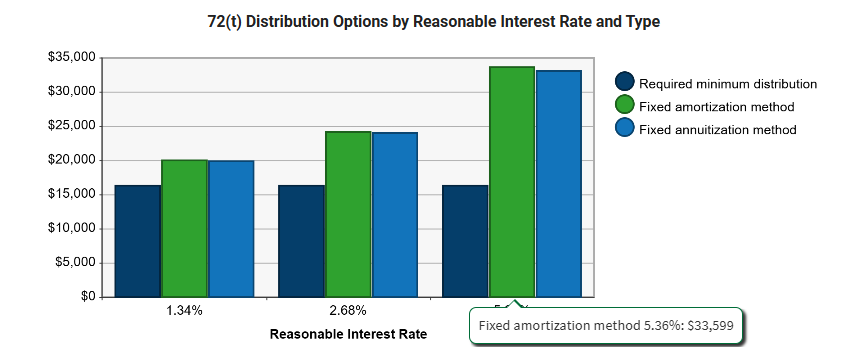

• Required Minimum Distribution (RMD) Method (variable withdrawals):

Under this method, the annual payment is determined based on the account balance and a life expectancy factor (single life, uniform life, or joint life). It is also variable in that it’s redetermined every year.

• Amortization Method (static withdrawals):

Under this method, the annual payment is amortized based on the life expectancy factor, the account balance, and the interest rate from Step #1. Once the amount is determined, it must be withdrawn every single year.

• Annuity Method (static withdrawals):

Under this method, you use the annuity factor based on age and the interest rate from Step #1. Once the amount is determined, it must be withdrawn every single year.

Using Amortization or Annuity methods are best, as they are static and require no recalculations every year.

> Account balance of your IRAs

You can determine the portion of your account subject to distribution. For example, say you have a 401(k) with a $1,000,000 balance. You can roll over that $1,000,000 into an IRA. From there, you can roll over, say, $500,000 into another IRA, which could be subject to the 72(t) plan.

An example will make much more sense, so let’s get into it!

Example

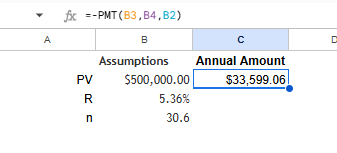

Say you will be 56 by the end of 2025. You have $1,000,000 in your IRA and transfer $500,000 of it to another IRA to be subject to the 72(t) rules. You choose the Fixed Amortization method and Single Life factor, as it results in the highest withdrawals. The interest rate is 5.36%.

The Single Life factor is 30.6:

The fixed amortization amount can be determined by using the PMT formula in Excel/Google Sheets.

You can also use a calculator to double check your values:

It matches my calculated value!

So, you can start withdrawing $33,599 per year (schedule these EXACT withdrawals every year) and must continue until you reach age 59½ or complete 5 years plus 1 day, whichever is LONGER. In our case, that would be the 5 years.

How do you actually establish the plan?

To establish the plan, it’s just a document that you can draft (I highly recommend running it by a CPA or a lawyer).

This document should describe all the assumptions, calculations, and include brokerage statements with amounts, dates, etc.

Tax time

From the tax form standpoint, you will receive a 1099-R from your custodian.

The most important part is to make sure that Box 7 has a “2” in it (the exception code for SoSEPP 72(t)). If it does, you don’t need to file Form 5329.

If it doesn’t, you will need to file Form 5329, “Additional Taxes on Qualified Plans.”

On line 1 and 2, you need to enter the amount you withdrew, and the exception number is 02.

Summary

This strategy allows you to access your retirement funds well before age 59½, but the rules are complicated. Make sure you consult a qualified professional.

I hope you enjoyed this & share this email with friends!

See you next Saturday.