Many people underestimate the financial impact of the Employee Stock Purchase Plan (ESPP) or don’t fully understand how it works. I hope to clarify how the plan works, how to enroll, and how to report it on your taxes.

What is an ESPP?

An ESPP is a benefit that allows employees to purchase company stock at a discount, usually up to 15%. The ESPP benefit is not offered by all publicly traded companies. Based on a 2021 study, roughly 38% of Russell 3000 companies offered this benefit.

Now, the rules vary significantly across companies. For example, here are some options companies offer:

- 15% discount at the end of the offering period

- 5% discount at the end of a 3-month offering period

- 10% discount with a “lookback provision” and no holding requirement

For example, I worked for a Fortune 500 technology company, and they offered a 15% ESPP with a “lookback provision” (which basically means that during an offering period (e.g. 3 months) you will purchase stock at the lower of the stock price on the offer date or the purchase date) and no required holding period (meaning you can sell immediately if there’s no need to hold for a certain period of time).

This is essentially free money if you can contribute.

Quick Example

Say you work for a company, and the share price is $100. Your company doesn’t offer a “lookback provision.” The discount is 15%.

> You will buy the stock at $85 during the buying period.

> If you sell immediately for $100 (assuming no required holding period), your profit is $100 – $85 = $15/share.

> $15 gain / $85 purchase price = 17.64% return on your money pre-tax. That’s pretty good!

Should you contribute to an ESPP?

It depends. It all comes down to the benefit offered.

For example, a good friend of mine has the following ESPP:

- 5% discount

- No lookback

- 1-month holding period

This is probably the worst ESPP plan out there.

In contrast:

- 15% discount

- Lookback provision

- No holding period

This is one of the best plans out there.

Personally, for the first one, I would not contribute. The juice isn’t worth the squeeze, and in 1 month of holding, anything can happen to the stock price, and your 5% discount might be “worthless.” For the second, I would put as much money as I can!

Maximum contributions

ESPP plans are specific to employers. This means that different plans have different limits.

However, if your company has a qualified ESPP, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a year.

The IRS looks at the value of the stock on the first day of the offering period toward the $25,000 limit, not the price you purchase it at.

For example, if the share price at the start of the offering period is $100, the IRS limit is 250 shares, even though you can purchase 294 shares ($25,000 / $85 with the 15% discount).

Keep in mind, though, that your company limit may differ from the IRS $25,000 limit, so check your plan documents.

Selling vs. holding

If I were participating in an ESPP plan, I would sell shares immediately after purchasing.

My reasoning is that holding employer shares presents an unnecessary risk (your paycheck comes from the same company as the stock you hold).

Yes, if you hold the purchased shares for a longer period, you can generally decrease the tax impact with a qualified ESPP plan (more on taxes in a bit), but what if the share price decreases from $50 to $15 in one year?

How does this fit into your $$ allocation?

We have limited resources (i.e. $$$). So, where do we put the ESPP in our investment allocation?

Obviously, how much to contribute (or even if you should contribute in the first place) comes down to the benefit provided by your employer (i.e. the discount %).

For example, say you have a 15% discount with no holding period. This is basically a 17% return on your money.

So, how would I go about my investment strategy if I have a 5% mortgage, a 5% car loan, no credit card debt, and a 6-month emergency fund?

I would:

1. Contribute to a 401(k) up to the match first. This is typically a 50–100% return on your investment due to the match.

2. ESPP to as much as I can (sell right away).

3. HSA.

4. Roth IRA.

5. Finish maxing out the 401(k).

6. Brokerage.

7. Pay off debt.

The rationale behind this strategy is that the ESPP provides a guaranteed 17% return (if your company offers a 15% discount), which beats the typical 8–10% average market returns.

Taxes & reporting

The taxes will depend on the type of ESPP plan. There are two main types:

- Qualified ESPP

- Unqualified ESPP

Approximately 79% of ESPPs are qualified, so I will focus on the qualified ESPP.

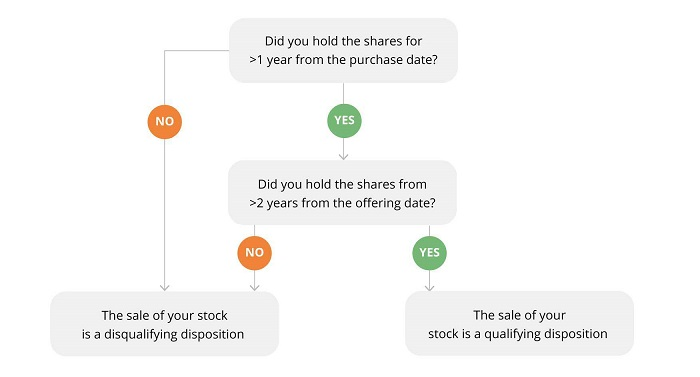

Now, if you have a qualified ESPP plan, the taxation will depend on whether the ESPP is a Qualifying Disposition or a Disqualifying Sale.

Here’s a simple chart to help you understand whether you have a qualifying or disqualifying sale:

If you have a disqualifying disposition, you don’t owe taxes at the time of purchase, but at the time of sale, the discount is taxed as short-term gains (ordinary income tax brackets).

If you have a qualifying disposition, you don’t owe taxes at the time of purchase either, and the discount is taxed as ordinary income using the price at the start of the offering period. Long-term capital gains applies to the remainder of your sale proceeds.

I believe that it’s not worth holding to receive the tax benefit and would recommend selling immediately. However, if you believe in your company’s future, it may work for you.

At the end of the year, you will receive a W-2 (which includes taxable income from the ESPP), Form 3922 (detailing information about the ESPP), and Form 1099-B (showing capital gain/loss on the sale). Here’s an amazing guide from Fidelity on how to file your taxes using these forms.

If you enjoyed this newsletter, would you please share it with a friend? I would really appreciate it.

Chat next week!

MC, CPA