There are many things you can do to lower your taxes, such as contributing to an HSA or 401(k), or taking advantage of tax credits.

I believe real estate is actually one of the best ways to lower your taxes.There are a few different loopholes with real estate that can lower your tax bill, but I want to discuss a strategy that doesn’t require much effort aside from owning a property.

Special allowance

The IRS has a special allowance that says, “If you actively participated in a passive rental real estate activity, you may be able to deduct up to $25,000 of loss from the activity from your non-passive income.”

What does this mean in simple language? You can take a maximum $25,000 deduction against your income, including W-2 income.

As with any IRS loophole, there are a few conditions to meet for this to apply:

- Actively participate

You must actively participate in the rental property. Active participation means you were involved in making management decisions, arranging for others to provide services (like repairs), approving new tenants, deciding on rental terms, etc. Essentially, it means you were involved in managing your rental property.

- Income limitations

If your modified adjusted gross income (basically all your income, such as interest, W-2, dividends, business income minus certain adjustments like student loan interest deduction and taxable social security) is $100,000 or less, you can deduct your rental property loss up to $25,000.

If your modified adjusted gross income (MAGI) is more than $100,000 but less than $150,000, your special allowance is limited to 50% of the difference between $150,000 and your MAGI.

If your MAGI is $150,000 or more, there is no special allowance, and you cannot take the deduction.

For example, let’s consider Josh. He earns a $95,000 W-2 salary and has no other income. His MAGI is $95,000, allowing him to take the maximum deduction of $25,000.

If Josh’s salary is $125,000 (making his MAGI $125,000), he can deduct $150,000 – $125,000 * 50% = $12,500, the maximum deduction of his rental loss.

If his salary is $175,000, he is not eligible for the deduction.

- Generate a loss on the rental property

At this point, you might be thinking, “I understand the rules, but how can my rental property lose money?”

Well, it all comes down to the depreciation deduction. Every year, you can deduct a portion of the reduced “paper” value of your property.

The IRS allows you to take a depreciation deduction equal to the building cost basis divided by 27.5 years.

For example, if you purchase a home in Indiana for $200,000 (with the land valued at $20,000), you can deduct approximately $6,545 in depreciation each year ($180,000 / 27.5 years). Additionally, you can deduct interest on the mortgage, utilities, and other expenses.

Many investors also do a “cost segregation study”, which accelerates depreciation, allowing for larger losses in the first year. As an example, that same property might be able to generate a ~$60,000 loss in year 1 through cost segregation and bonus depreciation.

This strategy could allow you to claim a $25,000 loss in year 1, another $25,000 loss in year 2, and a $10,000 loss in year 3, resulting in approximately $10,000-15,000 in tax savings!

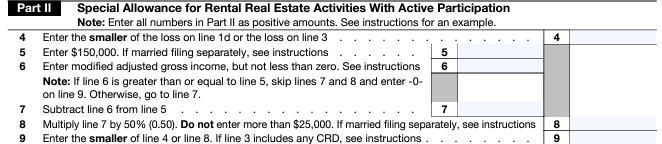

How do you take the loss?

When you file your tax return, you will be able to attach Form 8582, and Part II will calculate the deduction amount: