In this newsletter issue, I share a few strategies that can help you lower your taxes. Some of these strategies will provide an immediate tax benefit, while others may reduce the overall tax impact.

1. 401(k)

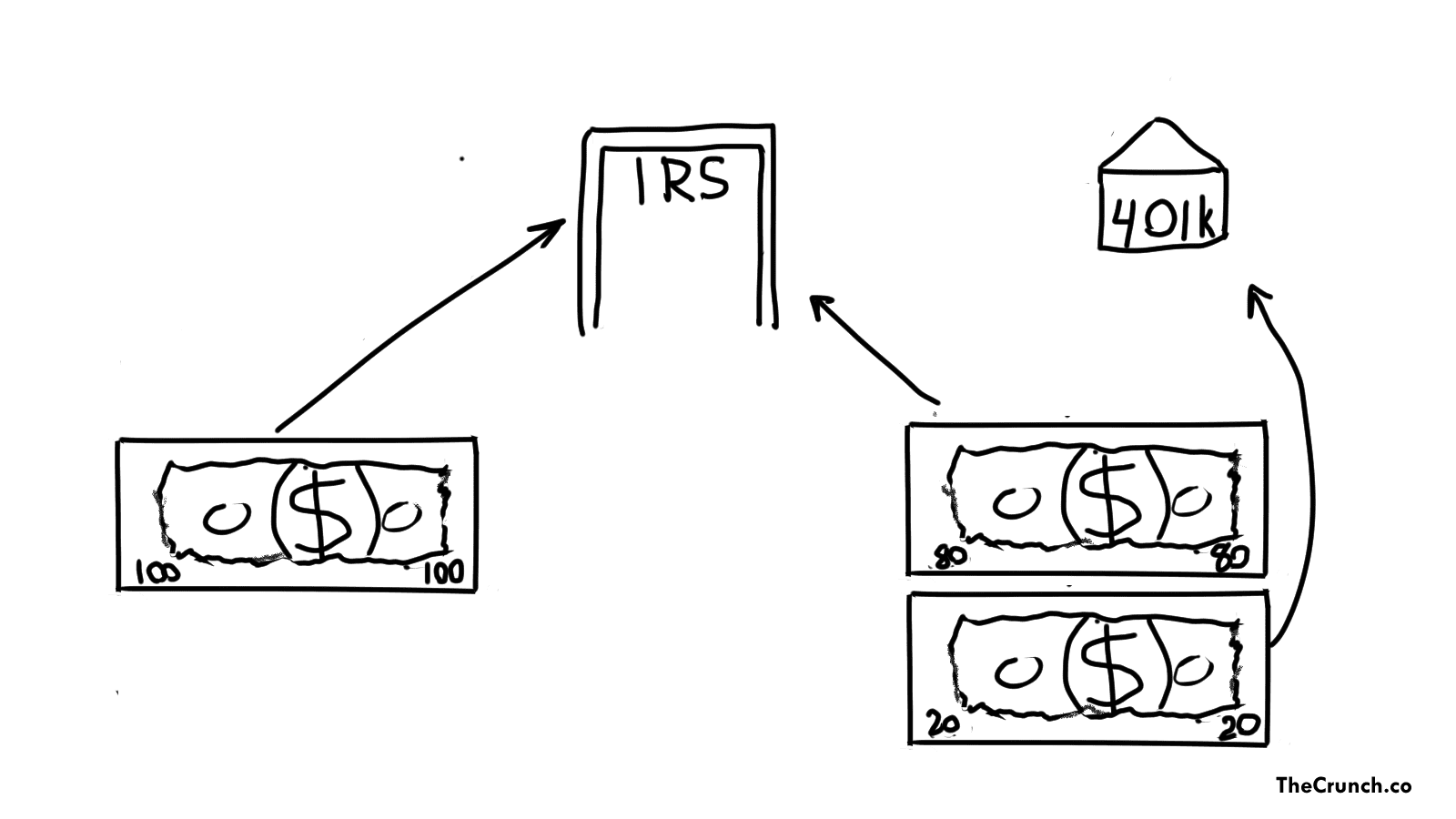

401(k) is a retirement savings plan offered by employers.

For example, let’s say you make $65,000 a year and put $5,000 into your 401(k). Instead of paying income taxes on the entire $65,000 you earned, you’ll only owe tax on $60,000 of your salary (excluding the standard deduction)

In other words, saving for the future lets you shield $5,000 from current taxation, saving around $1,000 in taxes.

To simplify, instead of 100% of your money being taxable, now only ~70-95% (depending on your contribution %) of it is taxable.

If your employer doesn’t offer a 401k, consider opening a Traditional IRA:

2. Traditional IRA is a retirement savings account.

Its primary purpose is to provide a tax advantaged way to save for retirement.

The tax deduction for contributions depends on:

- Whether you are covered by a retirement plan at work (i.e. 401k)

If you are filing as single and the Adjusted Gross Income (AGI) is less than $73,000, a full $6,500 deduction is allowed. If it’s more than $73,000 but less than $83,000, a partial deduction is allowed. If you make more than $83,000, no deduction is allowed.

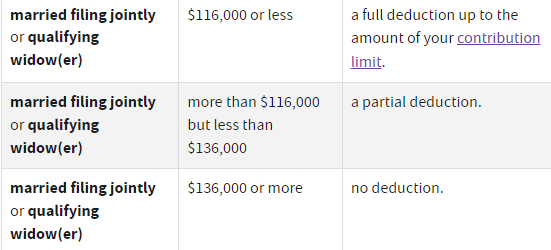

If you are marrying filing jointly, here are the ranges:

- If you are not covered by a retirement plan at work

If you are single, the income limit doesn’t apply. If you are married filing jointly and the spouse is covered by a plan at work, and the AGI is less than $218,000, a full deduction is allowed.

These limits are for the 2023 tax year, so the ranges might increase for 2024. They usually update them in September.

3. HSA

A Health Savings Account (HSA) is a tax savings account designed for people with high-deductible health plans. Per the IRS guidelines, an HDHP is a health insurance plan with a deductible of at least $1,600 for an individual plan, or $3,200 for a family plan.

Contributions to an HSA are made with pre-tax dollars (similar to 401k). Any interest or investment earnings within the HSA are also tax-free. Withdrawals from the HSA are tax-free if used for qualified medical expenses. So it provides a triple tax advantage (tax deduction, tax-free growth, tax free withdrawal)

The HSA contribution limits for 2023 are $3,850 for self-only coverage and $7,750 for family coverage. If you do qualify for it, contact your employer for enrollment.

4. Commuter benefits

If you commute to work, and your company has commuter benefits, this is a great way to save some money on taxes.

You contribute pre-tax dollars (similar to 401k) that you can use on your commute, and don’t have to pay taxes on the contribution. Since you were going to use some money on commuting anyways, this is a great option.

5. 529 Plan

529 plan is a tax-advantaged savings plan. The account offers tax-free earnings growth and tax free withdrawals for qualified educational expenses. The contributions are not tax deductible on the federal level, but might be tax deductible on the state level (depends on your state).

Also, starting in 2024, you can roll unused 529 assets, up to a lifetime limit of $35,000, into the account beneficiary’s Roth IRA.

There is a limit to the maximum contribution tax deduction for 529 contributions, and would depend on your state.

6. Capital loss rebalancing

Capital loss rebalancing is a process to sell a stock or ETF at a loss, and immediately repurchasing another stock/ETF. You cannot immediately buy back the same stock/ETF due to the wash sales rules. Here is a quick example:

- Let’s say you bought VOO (an S&P 500 index fund) for $480 (its all time high price as of this writing). Now, it trades for $460. If you sell your VOO for $460, you will generate a loss of $20 per share. If you had 100 shares, you will generate a loss of $2,000.

- Now, after selling, you would immediately go ahead and buy VTI, a total US stock market index ETF (or another stock/ETF). VOO and VTI have a 90% weight overlap, so they have similar performance.

- Overall, you generated a paper loss of $2,000 (that you can deduct on your taxes), and bought a very similar index fund, and wash sales would not apply.

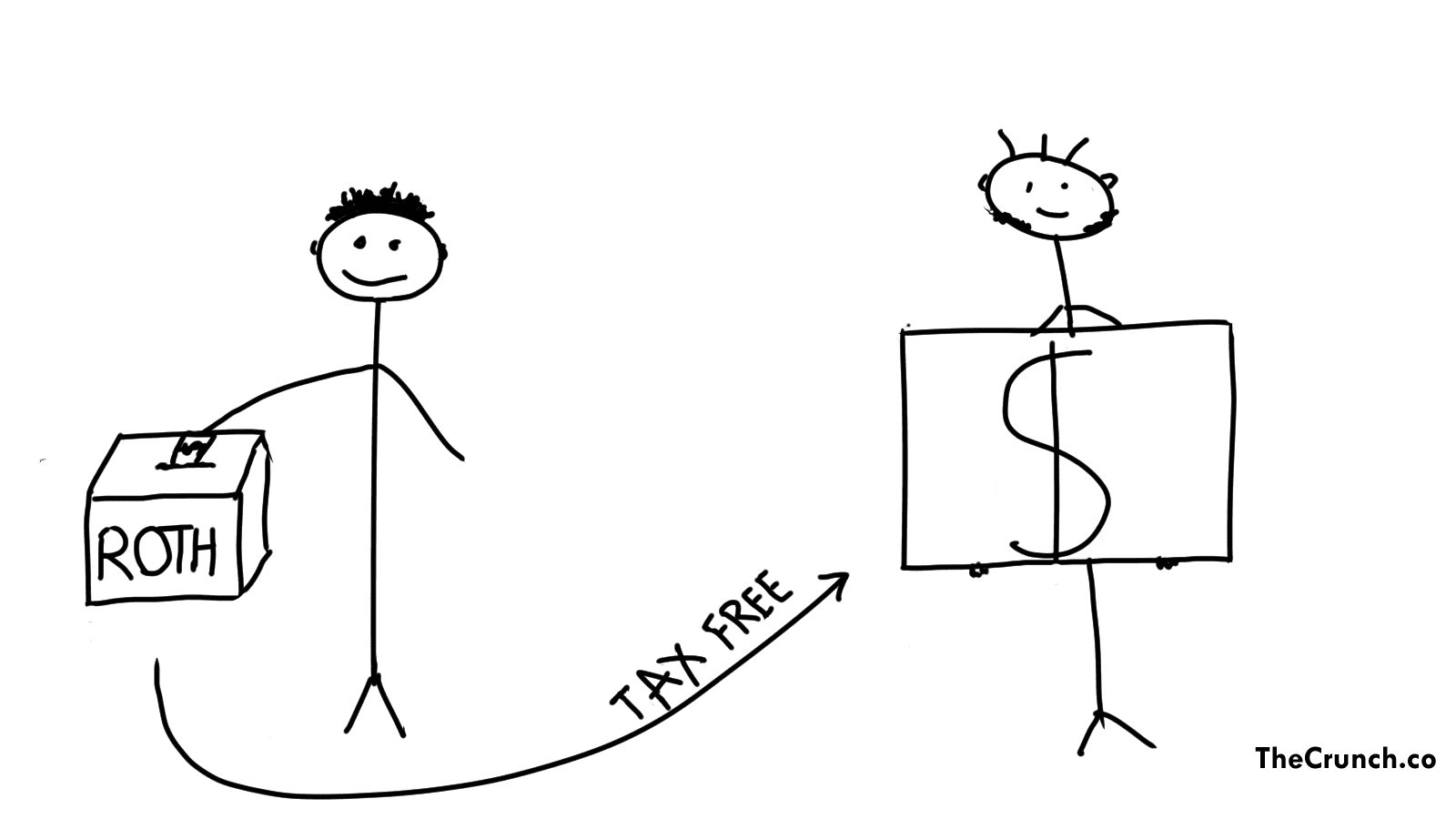

7. Roth IRA

Roth IRA is a retirement account that offers extreme tax benefits. Contributions to a Roth IRA are made with after-tax dollars, meaning there is no tax deduction for your contribution, but:

→ Tax-free withdrawal during retirement

→ Contributions (the money you put into the account) can be withdrawn at any time without taxes or penalties

→ No Required Minimum Distributions (RMDs)

→ Protection against tax rate uncertainty. Did you know that in the 1980s, the top marginal tax rate was 50 percent? We never know what will happen in the future. Roth IRAs protect us from uncertainty.

→ Withdrawals don’t count towards provisional income related to Social Security taxation.

→ Lack of Medicare premium increases since Roth IRAs don’t count toward income.

8. Mega Backdoor Strategy.

I shared about this strategy last week. It helps you shield even more money from future taxation.

9. Real estate and owning a business.

Ultimately, there’s only so much you can do with a W-2. Owning a business, or real estate, allows for a lot of tax strategies and deductions.

Any questions? You can always reply to this email and ask!

See you next Saturday.

MC, CPA