The savings account interest is dropping.

Many banks lowered their yields by 0.3-0.5%. Vanguard Money Market Fund dropped to 4.82%.

The yields will continue to drop as the Fed cuts rates. Today, I wanted to explore another interesting vehicle for savings: I Bonds.

What is it?

Series I Savings Bonds (also called I Bonds) are government-issued savings bonds that offer inflation protection.

Just like Treasury Bills, I Bonds are state and local tax-free.

The big benefit of I Bonds is that they are tax-deferred for up to 30 years.

This means that you keep accruing interest without paying any tax on that interest in the meantime. That’s a huge benefit for someone in a high-income tax bracket.

Rates

I Bonds have two components that make up their yield: a fixed rate and an inflation-adjusted rate.

The fixed rate is fixed for the entire duration of the I Bond. The fixed rate is announced twice per year—on May 1 and November 1. The current fixed rate is 1.30%. So, if you buy an I Bond now, you will receive a fixed portion of 1.30% for up to 30 years.

The inflation rate is based on the Consumer Price Index and is also announced on May 1 and November 1. The May rate is based on the change in CPI from September to March. The November rate is based on the change from March to September. The change applies to both newly issued I Bonds and existing ones.

Back when the I Bonds were first introduced, they were yielding ~6.31%:

Current rate is 4.28%:

The interest accrues every month and compounds semiannually. This means that every 6 months, you will see the bond’s value increase by the accrued interest for that 6-month period.

You must hold your I Bond for 12 months before redeeming and receiving the interest.

But if you cash in the bond in less than 5 years, you lose the last 3 months of interest.

Growth

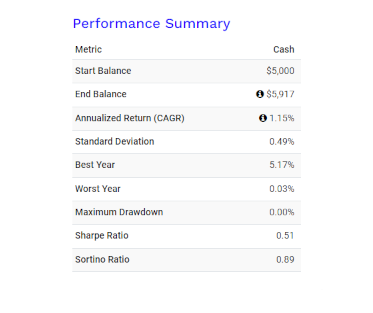

I wanted to compare buying $5,000 of I Bonds on January 1, 2010, versus storing your money in 3-month Treasury Bills or Treasury MMFs.

According to the TreasuryDirect calculator, the current value of the bond would be $7,682:

The treasury’s end value would be $5,917:

So, the difference is significant. This is mainly due to the fact that the T-bills didn’t yield much throughout 2010-2016.

In addition, you would have to pay tax on the $900 of interest from Treasury, while that’s deferred with the I Bond.

How do I buy it?

I Bonds are sold at face value, meaning that you would pay $1,000 for a $1,000 I Bond.

You can buy I Bonds directly from TreasuryDirect.

The maximum purchase limit is $10,000 in a calendar year per SSN.

You can also get a $5,000 paper I Bond per SSN using your tax refund.

Savings bonds can also be owned by entities (trusts, estates, corporations, partnerships). Entities can open accounts on TreasuryDirect and purchase I Bonds there as well.

The $10,000 limit applies per entity.

Tax Benefits

As I mentioned, I Bonds are tax-deferred, meaning that the interest becomes taxable when you redeem the bond.

This could be helpful in situations when you are in a high tax bracket, making lots of money, and can avoid paying tax during those years. Then, in 30 years, during retirement, you can redeem the bonds and have only a minimal impact on your tax liability.

If you expect to be in a high tax bracket when you redeem I Bonds, they may not be the best vehicle to hold.

For this reason, if you expect to be in a high tax bracket when you redeem your I Bonds, they may not be a suitable investment for you. If you’re in your 20s now, in 30 years you might be in your peak earning years, likely placing you in a higher tax bracket when the bonds mature.

Quick Tip

I Bonds earn the full month’s interest if you own them on the last day of that month.

So, it’s generally a good idea to buy them at the end of the month, after also earning interest in MMF/Treasury/HYSA.

Alternatively, you may want to redeem them at the beginning of the month.