If you receive a windfall, a bonus, or maybe you were saving for something but plans changed, how would you invest the cash?

Would you invest it all at once (lump sum investing), or would you invest a portion every month or week (dollar cost averaging)?

I looked at some research studies to help make that decision:

This research paper was one of the first on this topic. The idea is simple – if you believe that the market goes up over time (as it generally has done over the past 100+ years), waiting to invest that money (DCA) is mathematically “suboptimal,” so you should invest it all at once.

By keeping money in high yield savings account or money market fund, you are betting against a market that is historically biased toward growth. The only way a “rational” investor could prefer DCA is that they believe the market will significantly drop. Duh… If only we knew when that would happen…

I mean, looking back, the S&P 500 has hit a new all time high 204 times so far in the last 10 years. But when will it take a pause?

2. Cost Averaging: Invest Now or Temporarily Hold Your Cash

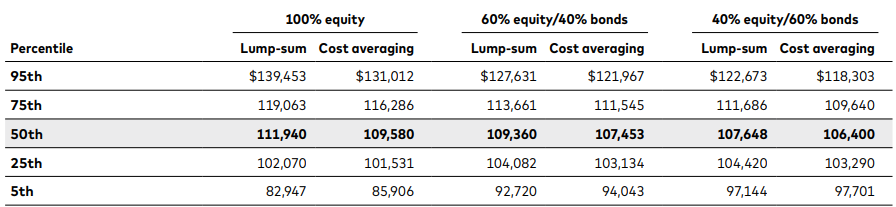

Say you have $100,000. You can invest it all at once or split it into three equal parts and invest each part one month apart. What would it be worth in exactly one year?

Vanguard ran this calculation using the Total Market Indexes for the years 1976 to 2022, analyzing various historical periods. They found that, regardless of the portfolio allocation, lump sum investing outperformed cost averaging most of the time:

You can also run a similar projection using portfolio backtesting websites.

For example, if you invested $10,000 in VTI on January 1, 2025, by December, you would have ~$11,709

What if you instead invested $833/mo for 12 months? You would have $11,147, or about $562 lower.

But if of course, the S&P 500 has been trending upwards in 2025, so this makes sense. But what happens in a declining market?

Cost averaging hinders portfolio growth in rising markets, but it provides protection in downturns.

Unfortunately, we don’t know what will happen in 2 weeks, 6 months, or 2 years with the stock market. This is why we have to rely on the data.

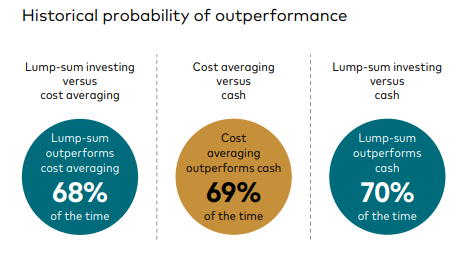

According to Vanguard’s research, lump sum investing outperforms cost averaging 68% of the time:

The numbers are clear. But what if you want to avoid big losses and are okay with sacrificing some growth?

This is where a 2012 research paper, titled “Dollar-cost averaging just means taking risk later” could be helpful.

Risk averse investors don’t care about averages. They care about worst case scenario, and potentially feeling regretful by using a lump sum investment.

In this study, out of 1,021 12 months investment periods, lump sum investors would see a decline during 229 periods (22.4%), while DCA would see such declines in only 180 periods (17.6%). On a $1,000,000 investment, the average loss was ~$84,000 for the LCI, vs ~$57,000 in the 180 DCA periods.

Of course, historical averages are only a guide. It is possible for LSI or DCA to underperform, or even lose a lot of money in any given period of time.

Bringing it back

In general, the research papers suggest that investing all at once may be the best strategy based on historical backtesting studies. It’s also important to look at your investment timeframe. If you need invested capital in 10 years vs 30 years, it could drive your decision as well.

Of course, before investing anything you should have an emergecy fund, and figured out what your goals are in the foreseeable future (e.g. are you planning to buy a house)

But if you do have some capital to put towards the market, receive an inheritance, or a substantial bonus, these studies could help inform to the decision making.

While most of us won’t win the lottery or inherit a substantial amount, one practical application to go with the lump sum investing strategy is to “front-load” your 401(k). If possible, an investor could significantly increase their 401(k) contributions until the account is maxed out early in the year. But you also need to consider any matching contributions you receive, as some companies don’t match if you don’t contribute.

My final thought

Ultimately, regardless of whether you choose dollar-cost averaging or lump sum investing, one thing is clear: you have to invest.

Having a plan for investing cash is the most important part. Choosing one strategy over the other will only make a marginal difference compared to keeping cash long-term.

I hope you enjoyed this one and learned something new.

See you next Saturday.