I see all over social media people making basic investment mistakes. Today, I wanted to share 3 quick lessons:

- Allocation

People often just copy the investment strategy of others. They look at social media and say, “oh, I will just copy what’s working for this person” or look and say “this CPA is putting his money in X, let me just do that too.”

But it’s important to determine the mix of investments that will work for YOU.

A lot of your portfolio should be dependent on your goals, risk appetite, your career (e.g. how “risky” it is), how far away you are from retirement, etc.

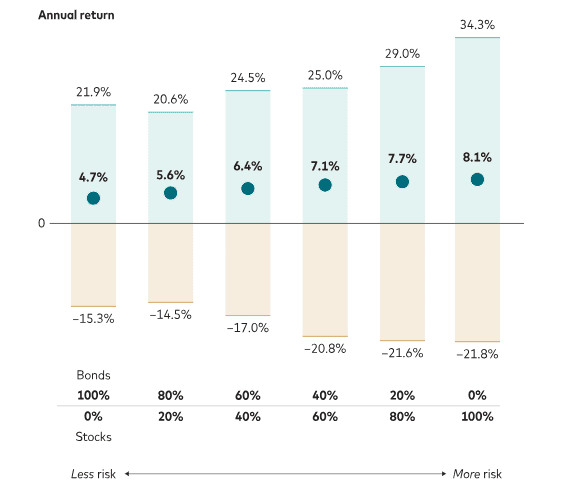

If you are young, you can take on more risk to achieve your goals, and you can reduce risk as you get closer to reaching your goals. I really like this chart:

It shows the top 5%, bottom 5%, and average annual returns for global stock/bond allocations from 1901-2022.

For example, the top 5% return was 34.3% for a 100% equity portfolio. But for a 60% stocks / 40% bonds portfolio, it was just 25.0%, or almost 30% lower. But it’s also more risky.

Are you okay potentially losing 21.8% in just 1 year with a 100% equity portfolio? You may be, depending on a lot of factors.

TLDR: invest based on YOUR goals and risk appetite, not others.

2. Cost

Whatever you choose to invest in, always pay attention to the expense ratio.

I personally don’t own a single fund with an expense ratio higher than 0.1%.

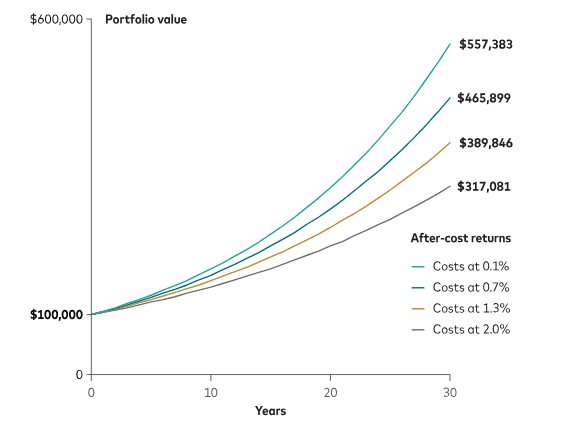

This chart will help you understand the impact:

Going from a 0.1% expense ratio to a 0.7% expense ratio is a $91,484 difference over 30 years. Small percentage points in the grand scheme of things, but they make a huge difference.

Yet I personally know people who pay these fees to invest in actively managed funds that provide minimal growth.

I understand that with a 401(k), you might not have many options, but many companies often offer Vanguard or Fidelity funds, which typically have the lowest fees. Make sure to review your options.

If you quit your job, you can roll your 401(k) balance into a rollover IRA to buy cheaper investments (e.g., VTI with a 0.03% expense ratio). However, this could impact your Backdoor Roth strategy if you are a high earner.

3. Discipline

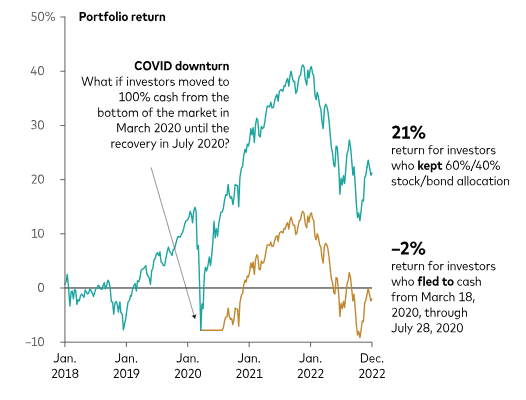

If you panic in the stock market, you will lose.

For example, if you moved to 100% cash at the bottom of the COVID downturn, you would have received a -2% return, compared to a 21% return if you had stayed consistent with your plan:

If you are selling, why?

Before investing, you should have a 3–6 month emergency fund if you are in the accumulation stage. More in retirement.

If you panic, it also means you don’t have an appropriate asset allocation, aren’t properly diversified, or don’t fully understand what you’re investing in.

Go back to figuring out the asset allocation YOU are comfortable with.