All over social media, we see statements like, “Invest in X, it will make you money” or “Buy this ETF, it’s the best!”

However, just because something works for someone else doesn’t mean it will work for YOU.

In this newsletter, I want to discuss how to create your own investment plan.

Before you start investing or creating your plan, it’s important to have an emergency fund in place first.

Let’s get started:

- Asset allocation

You need to determine the asset allocation for your investment plan, which involves two key components:

1a. Allocation between stocks and bonds

1b. Allocation for international investments

For the stock and bond allocation, I really like the Vanguard Investor Questionnaire. It asks a series of questions to help determine your ideal allocation. For example:

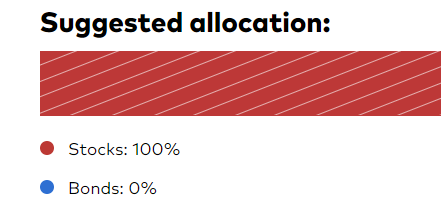

For me, I’m 100% in stocks and 0% in bonds. As a general rule of thumb, many people suggest holding 0% bonds until age 30, but it ultimately depends on your risk tolerance and comfort levels.

1b. International stocks

There are many arguments both for and against investing in international stocks.

100% US allocation:

- American exceptionalism

- US companies do business globally

- Maximizing returns may not be the highest priority for some international markets

20-40% International allocation:

- Neither US nor International stocks have shown consistently superior returns over the last 70 years, post-WW2

- Holding some international stocks is like adding insurance

- Provides a good portion of the diversification benefits of non-US markets

Ultimately, you will need to decide whether investing in international stocks is beneficial for you.

- Investments

The next step is to select the best investments to fulfill your asset allocation.

There are many different types of stocks – small-cap, large-cap, mid-cap, and various industries.

So, which one is the winner? No one knows.

That’s why I, along with many others, believe it’s better to invest in the entire market rather than trying to pick individual winners. This is where Total Market ETFs come into play.

Here are some ETFs that represent the US market:

• $VTI – Vanguard Total US Stock Market ETF (100% US)

• $FSKAX – Fidelity Total US Stock Market ETF (100% US)

• $SWTSX – Schwab Total US Stock Market (100% US)

For the international market:

• $VXUS – Vanguard Total International Stock Index Fund ETF (100% International)

For a mix of US and international markets:

• $VT – Vanguard Total World Stock Index Fund ETF (60% US, 40% International)

For bonds:

• $BND – Vanguard Total Bond Market Index Fund ETF (100% bonds)

Different companies offer different funds, but I prefer Vanguard funds because of their low expense ratios. Vanguard charges extremely low management fees for managing these funds.

Whatever you choose, make sure the expense ratio is no higher than 0.2%; if it is, consider looking for alternatives.

For example, if you’re 100% in stocks and have decided on an 80% US and 20% international allocation, you could invest 80% in $VTI and 20% in $VXUS.

- Account

In terms of account types, you should prioritize tax-advantaged accounts first, such as Roth IRA and 401(k). Once you’ve reached the contribution limits, the next step is to invest using a taxable brokerage account.

- Fees & taxes minimization

It’s important to minimize taxes strategically across your accounts.

For example, holding bonds in a taxable account is not tax-efficient because the interest they pay is taxed at ordinary income rates.

In contrast, holding bonds in a tax-deferred account, like a 401(k), is more tax efficient since you aren’t paying taxes on the interest income.

If your allocation is 80% stocks (100% US) and 20% bonds, you could hold $VTI in your taxable brokerage account and $BND (or a similar bond ETF) in your tax-deferred account.

As I mentioned before, pay attention to expense ratios – they make a huge difference.

- Rebalancing

Usually, you should rebalance your portfolio once a year to ensure it stays aligned with your ideal asset allocation. To minimize taxes when rebalancing, use dividends and new money inflows instead of selling assets.

Additionally, if this is your first time following the plan, it’s generally not recommended to take a significant tax hit by selling your current investments in a taxable account, unless the impact is minimal.

I know this is a lot to unpack, but you really need to consider these aspects to become a better investor. Don’t just follow the crowd (or even what I do) – come up with a plan that works for you.

MC, CPA