Retirement accounts are a great way to invest.

But many people, especially young professionals, don’t know where to put their money. With so many options available, it can be hard to know where to begin!

There are two main options available in your 401(k)/403(b) account:

1. Target Retirement Funds

These are funds that match your planned retirement year and automatically re-balance to become more conservative and less risky over time.

Sometimes, your 401(k)/403(b) provider might automatically enroll you in one of these based on your retirement age. For example, Vanguard has:

- Vanguard Target Retirement 2070 Fund

- Vanguard Target Retirement 2065 Fund

- Vanguard Target Retirement 2060 Fund

- etc

I personally don’t like them, as I believe they are too conservative.

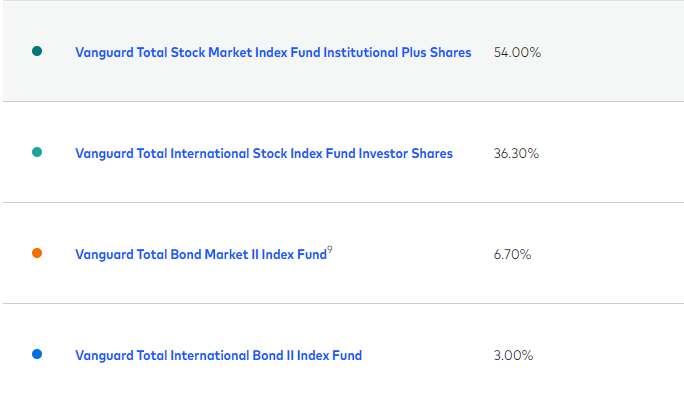

For example, Target Retirement fund of 2065, which is 40 years from now, is invested in:

So, almost 10% of the fund’s assets are invested in bonds.

In my opinion, there is no reason why a 23-year-old should be invested in bonds. They have 40 more working years and should be aggressive with their portfolio to maximize returns.

Now, if you are 50 years old and have:

- Less time to recoup severe losses

- More wealth to protect

It probably makes sense to add bonds to your portfolio to minimize risk exposure. If being conservative fits your personality and investing style, Target Funds might be a good option, but I believe there are better ways to invest in your 401(k).

2. Invest on your own

401(k) plans also allow you to select the funds you want to invest in.

This is the option I prefer, as you can select good funds with low expense ratios. For example, here are the 401(k) options available to me:

American Europacific Growth R6 (RERGX)

Artisan Mid Cap Fund Invest CL (ARTMX)

Blackrock Extended FD CL K (BEEMT)

Blackrock MSCI ACWI EX CL M (BMSIT)

DFA U.S. Sustainability Core 1 (DFSIX)

Dodge & Cox Intrntl Stk CL X (DOXFX)

Fidelity Advisor Real Est CL A (FRINX)

Fidelity Real Estate IDX INSTL (FSRNX)

Hotchkis and Wiley SML CP VL I (HWSIX)

JP Morgan Emerging Markets EQT R6 (JEMWX)

JP Morgan Large CAP growth R6 (JLGMX)

JP Morgan Mid CAP VAL FD R6 (JLGMX)

MFS INTERNATIONAL NEW DISCOVERY FUND (MIDAX)

MFS VALUE FUND CLASS A (MEIAX)

VANGUARD EXPLORER FUND (VEXRX)

VANGUARD INSTITUTIONAL 500 INDEX TRUST (VLCSP)

When you look at this list (yours might be something similar), it can be overwhelming. This is why many people opt for the target fund route, but here is how I go about selecting them:

The first step I take is to look for funds from Vanguard and Fidelity. They have the best funds with the lowest expense ratios. Schwab and T. Rowe Price also offer good funds.

The S&P 500 and Total US Market funds have performed extremely well in the past. If you have multiple options available, such as Vanguard 500 Index Trust and Fidelity 500 Index, select the one with the lowest expense ratio.

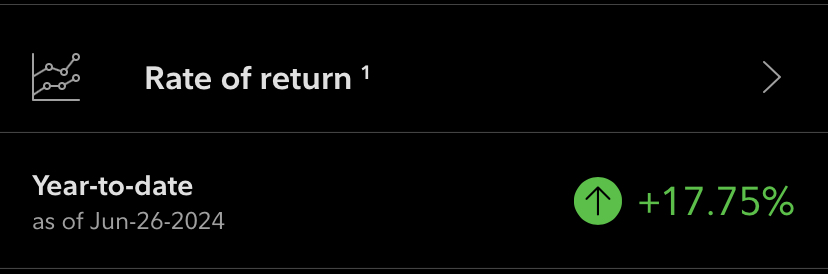

Out of that list, I’m 100% invested in the Vanguard Institutional 500 Index TR:

And the year-to-date returns are amazing:

Some people might add bonds to their portfolio too, but that depends on your age and risk tolerance.

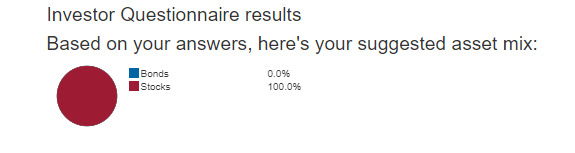

I really like this Vanguard questionnaire that can help determine a rule-of-thumb allocation between stocks and bonds. Here is my result:

And this is why I’m 100% invested in stocks!

Any questions or comments? Just hit that reply back!

See you next Saturday.

MC, CPA