A reader asked “Which strategy can high income earners use to save money on taxes?”

Today, I want to discuss a very underutilized strategy called the Mega Backdoor Roth that can be a great fit for high earners, especially before the end of 2024.

Mega Backdoor Roth

Mega Backdoor Roth is a strategy that allows funding Roth accounts far in excess of normal limits.

For example, say you are a higher earner and already max out your Roth IRA account (through Backdoor conversion), max out your 401(k) of $23,000 per year, and receive a $10,000 employer match.

Now, this strategy allows you to contribute an additional $36,000 into a Roth account. ($69,000 is the annual 401(k) limit, minus $23,000, minus $10,000).

This strategy could be a great way to get as much money as possible into a Roth (money grows entirely tax-free) before investing additional amounts in a taxable brokerage.

How does it work?

This strategy is only available through the 401(k) retirement plan. However, if your employer does not allow for after-tax contributions (particularly because of the nondiscrimination testing rules), you cannot use this strategy, so ask your HR first. Business owners can also use a Solo 401(k) if allowed by the plan.

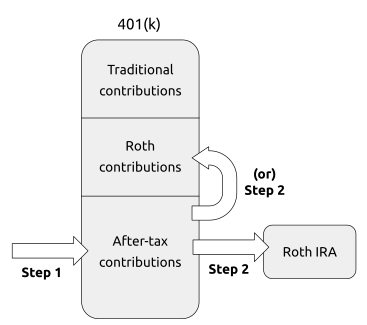

It’s a 2 step process:

- Contribute to a 401k after-tax account (don’t confuse it with the Roth 401k)

- Roll the funds over to the Roth IRA or Roth 401k

Here is a simple visualization of it:

The rules will usually vary from plan to plan, and how they label their accounts, so it’s also important to check your Summary Plan Description.

For example, here is a screenshot with the Mega Backdoor Roth option enabled. We can see the Pre-tax (Traditional 401k), Roth (Roth 401k), and traditional after-tax (Mega Backdoor).

Why would someone do this?

- Large contributions to Roth account (ability to contribute $40,000+)

- Further growth is all tax free

- Protected from creditors under ERISA

Where should I roll?

Step 2 requires you to roll the after-tax contribution into either a Roth 401k or a Roth IRA.

So, which is better?

First of all, your plan might only allow you to roll into a Roth 401k, so it’s important to check that first.

But if you have both options available, here are the benefits of each:

- Roth 401k – Allows minimizing taxable earnings by automatic conversion and might be easier to set up.

- Roth IRA – Offers a greater variety of investment options and has flexibility of withdrawals (can withdraw contributions penalty-free at any time).

In my opinion, rolling into a Roth IRA is a better option, but a Roth 401k works well too.

Earnings

When you contribute to after-tax (step 1), the amount is automatically invested. Then, when you roll the balance into a Roth IRA (step 2), you might have some earnings. These earnings are taxable income.

To reduce the taxable amount, do steps 1 and 2 as soon as possible. Some plans might offer automatic rolls or the option to invest in a Money Market Fund to minimize earnings.

Some employers might issue separate checks to split the contributions and earnings. In that regard, you might put the after-tax contributions into a Roth IRA and the earnings into a Traditional IRA to avoid paying taxes. But be careful, as contributing to a Traditional IRA might affect your Backdoor Roth strategy if you are using one.

Example

Say you have $5,000 in your Roth IRA and contributed $10,000 to the after-tax 401k account (step 1). You then roll it into a Roth IRA (step 2). Assume there was $100 in earnings earned between steps 1 and 2.

You can roll $10,100 into the Roth IRA and pay taxes on the $100. Your total Roth IRA account will be $15,100, or roll $100 into the Traditional IRA (no tax impact) and roll $10,000 into the Roth IRA. Your total Roth IRA account will be $15,000.

Reporting

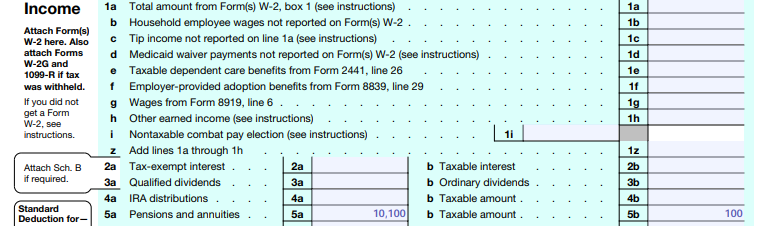

By the end of the year, you will receive a 1099-R form that you will need to report on your taxes.

In our prior example, if you roll $10,100 into the Roth, your Tax Form 1040, Line 5a, will be $10,100, and Line 5b will be $100.

If you rolled $10,000 into a Roth and $100 into a Traditional IRA, Line 5b will be $0, with no tax impact.

If you are using a tax preparer, tell them exactly what you did so they can report it correctly. By the way, using Form 1040, Lines 5, is exactly how you can double-check whether they did it right.

I hope you enjoyed this one. If you have any feedback, just respond to this email.

See you next Saturday.

MC, CPA