I was recently asked “What are some strategies available to high earners to potentially minimize their taxes?”

Of course, we have our typical options, like 401ks, HSAs, Roth IRAs, or more sophisticated strategies with real estate/business planning. But for many high earners, you may also be able to take advantage of the “Mega Backdoor Roth” (MBDR) option.

Mega Backdoor Roth

MBDR is a strategy that allows you to fund Roth accounts far in excess of the normal contribution limits.

For example, say you are a higher earner and already max out your Roth IRA (through “Backdoor Roth” conversion), max out your 401(k) of $24,500 per year, and receive, say, a $5,000 employer match.

This strategy allows you to contribute an additional $42,500 to a Roth account.

This is because the total 401(k) contribution limit in 2026 is $72,000, including employee contributions, employer contributions, and after-tax contributions. Subtracting the $24,500 employee contribution limit and the $5,000 employer match leaves $42,500 available for after-tax contributions. If you are over age 50, the limits go even higher, with an additional $8,000 catch-up contribution available.

This strategy could be a great way to get as much money as possible into a Roth before investing additional amounts in a taxable brokerage.

How does it work?

An important caveat is that this strategy is only available through the 401(k) retirement plan, and your plan may not allow it. Small business owners may use a Solo 401(k) plan to potentially use this strategy too. Data from Fidelity Investments show that only about 11% of employer-sponsored 401(k) plans permit MBDR conversions.

Your employer needs to allow “after tax” contributions in order to contribute.

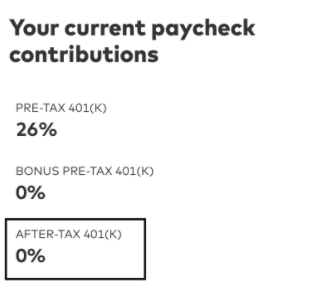

For example, if you log into your 401(k) and try to change to contribution %, you should see something along the lines of “After-tax 401(k)” if your plan allows it:

(Don’t confuse the “after-tax” with a Roth 401(k) option)

If you see this option, you can likely utilize the MBDR strategy.

It’s a 2 step process:

- Contribute to a 401k after-tax account

- Convert the funds over to the Roth IRA or Roth 401k (depending on the available options)

The rules will usually vary from plan to plan, so it’s also important to check your Summary Plan Description.

Why would someone do this?

Say a high earner maxed out their pre-tax 401(k), and did a backdoor Roth conversion. They are thinking of contributing to a traditional brokerage account or doing the mega backdoor strategy.

Some benefits for the latter:

- Further growth is all tax-free (instead of potential capital gains with brokerage account once sold)

- No taxes on dividends (which could be $$$ for high earners, especially those living in high-tax states)

- Easy rebalancing opportunities (not taxes when you sell & rebuy within the Roth account)

- Potentially protected from creditors under ERISA

Some benefits for the brokerage account:

- Flexibility (No contribution limits, no withdrawal rules, no age restrictions). This is a big one. There are rules around withdrawals from retirement accounts, so it’s important to analyze your personal retirement goals

- If your plan has bad/expensive funds, you’re locked into them with MBDR (likely shouldn’t be an issue since most plans that offer MBDR have decent options)

Where should I roll?

Generally, you may have the option to put your after-tax dollars into Roth 401k or Roth IRA. If you have both options available, some benefits of each include:

- Roth 401k – can minimize taxable earnings by automatic conversion, and might be easier to set up

- Roth IRA – greater variety of investment options and has more flexibility of withdrawals (can withdraw non-taxable conversion part penalty-free).

In my opinion, rolling into a Roth IRA is a better option, but a Roth 401k works well too.

Earnings

When you contribute to after-tax (step 1), the funds are generally invested automatically. Then, when you roll the balance into a Roth IRA (step 2), you might have some earnings. These earnings are taxable income.

To reduce the taxable amount, do steps 1 and 2 as soon as possible. Some plans might offer automatic rollovers.

Example

Say you have $5,000 in your Roth IRA and contributed $10,000 to the after-tax 401k account (step 1). You then roll it into a Roth IRA (step 2). Assume there was $100 of earnings between steps 1 and 2.

You can roll $10,100 into the Roth IRA and pay taxes on the $100.

Reporting

By the end of the year, you will receive a 1099-R form that you will need to report on your taxes.

In our prior example, if you roll $10,100 into the Roth, your Tax Form 1040, Line 4a, will be $10,100, and Line 4b will be $100.

If you are using a tax preparer, tell them exactly what you did so they can report it correctly.

I hope you enjoyed this one. If you have any feedback, just respond to this email.

See you next Saturday!

MC, CPA