Before we dive into today’s topic, I have a quick favor to ask.

Over the past 35 weeks, I’ve written 35 issues on The Crunch about various topics (investing, budgeting, taxes, etc).

My question to you is: what is your feedback? What topics would you like me to cover? Simply respond to this email and tell me what you think. I want The Crunch to be the best personal finance resource, and your feedback matters.

By the way, this topic suggestion came from another subscriber, so thank you, Andrew! Let’s dive right in.

If you have savings for a house down payment, a car, or just an emergency fund, where do you keep them?

The 2 most popular ways are Money Market Funds and High-Yield Savings Accounts. But which one is better?

MMF

A Money Market Fund is simply a mutual fund that invests in treasury bills, short-term government obligations, and other low-risk agreements.

The fund tries to maintain its share price at $1.00. So, if you deposit and buy $5,000 worth of MMF, you will receive 5,000 shares. When you sell the 5,000 shares of an MMF, you will receive $5,000.

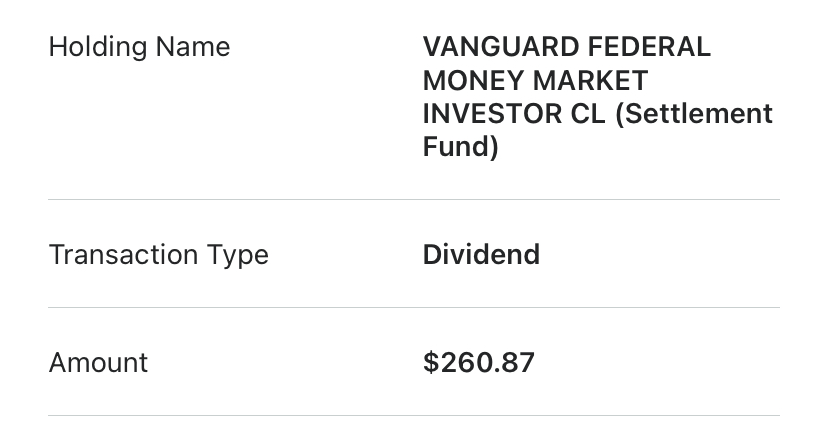

Every month, MMFs pay you a dividend (essentially a monthly interest) based on the yield:

Big brokerages (Fidelity, Vanguard, Schwab) have their own Money Market Funds that you can purchase within their brokerage accounts. These funds have billions of dollars invested in them (e.g., VFMXX – $310B as of 8/31/2024).

For example, Vanguard has the Vanguard Federal Money Market Fund. (VMFXX – 5.21%).

Fidelity has Fidelity Government Money Market Fund (SPAXX – 4.96%)

Schwab has Schwab Government Money Fund – Investor Shares (SNVXX – 4.98%)

Some banks or credit unions offer Money Market Funds, but they typically don’t yield as much as buying directly from a brokerage. When looking at the yield, always check the 7-day SEC yield, which is the yield after fund fees.

There are also different types of Money Market Funds (Government, Treasury, Municipal). I covered them more in depth here.

What about HYSA?

HYSA is just a high-yield savings account.

Typically, big banks like Chase or Bank of America don’t pay much interest since they don’t really need to attract new clients. Other banks offer higher yields to attract more customers.

Here are some examples:

BMO Harris – 5.10% (select markets)

CIBC – 5.01% (minimum $1,000)

CIT Bank – 4.85% (minimum $5,000)

So… MMF or HYSA?

I can’t answer this for you, but I can help guide you through the decision:

- Are you comfortable with a small level of risk?

The big benefit of the HYSA is that it’s FDIC insured. So, if anything happens to your bank, your money is secured up to $250,000 per account holder. Your money is safe.

The biggest risk for an MMF is if its share price drops below $1.

The last time an MMF dropped below $1 was during the 2008 financial crisis, so it’s technically possible. Luckily, the SEC recently adopted money market fund reform to enhance the stability of these funds. The reform increased minimum liquidity requirements for MMFs to provide a more substantial liquidity buffer in the event of rapid redemptions.

Personally, I’m comfortable with this risk and have a substantial portion of my emergency fund/savings in a Vanguard Money Market Fund.

2. What is the interest yield?

If your bank pays you 4% interest vs. Vanguard MMF paying 5.21%, is the extra 1.21% interest yield enough to justify switching to an MMF?

What if you have a 5.00% HYSA vs. a 5.21% MMF? Is 0.21% enough to justify the extra (even if small) risk?

- How will taxes impact the return?

Generally, MMFs and HYSAs are taxed in the same way. You receive monthly interest/dividends, and at the end of the year, you will receive a 1099-INT (bank) or 1099-DIV (brokerage). The tax impact is the same.

This is unless you purchase a Treasury (state/local tax-exempt) MMF or Municipal (federal tax-exempt) MMF. Currently, the Vanguard Treasury MMF yields 5.19% and is state/local tax-exempt. That’s a huge benefit over an HYSA if you live in a state with high income tax.

4. How much money am I working with?

If you have a $5,000 emergency fund, the difference between a 4% HYSA and a 5.20% MMF is $60/year. In this case, is it worth changing? For some, it might be; for others, perhaps not.

If you have a house down payment fund of $50,000, the difference is much larger.

I hope these questions can help you decide. Needless to say, I hope you aren’t receiving 0-2% interest on your savings—there are better options!

See you next Saturday.

MC, CPA