Retirement is a number in your investment account, not an age. Planning for retirement early on will ensure comfortable living later down the road. But how do you actually plan for it? When is enough, enough?

This is where the Trinity Study comes in (many people don’t know, but this is where the 4% Rule came from!)

The Trinity Study explored the historical success of various withdrawal rates from portfolios of stocks and bonds. Is withdrawing 7% from your portfolio every year safe? Is 3% the right amount?

The goal of the study was not to determine an absolute rate for every single investor (since factors like risk aversion, the desire to leave a large estate to heirs, and market fluctuations impact the rate), but rather to determine a withdrawal rate for planning purposes ahead of time.

The study measured the impact of withdrawal rates ranging from 3% to 12%. For example, if you have a $300,000 portfolio, using the 3% withdrawal rate, you would withdraw $9,000 per year, or $36,000 if using the 12% withdrawal rate.

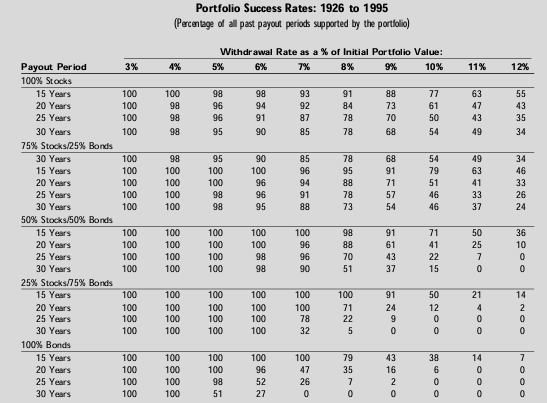

So, here are the success rates of these withdrawal rates using historical returns from 1926 to 1995:

We can see that if you have a portfolio with 50% stocks and 50% bonds, withdrawing 4-5% has a 100% success rate based on historical averages from 1926 to 1995. While future averages might not match those of the past 20-30 years, this measure is still a reliable method for testing.

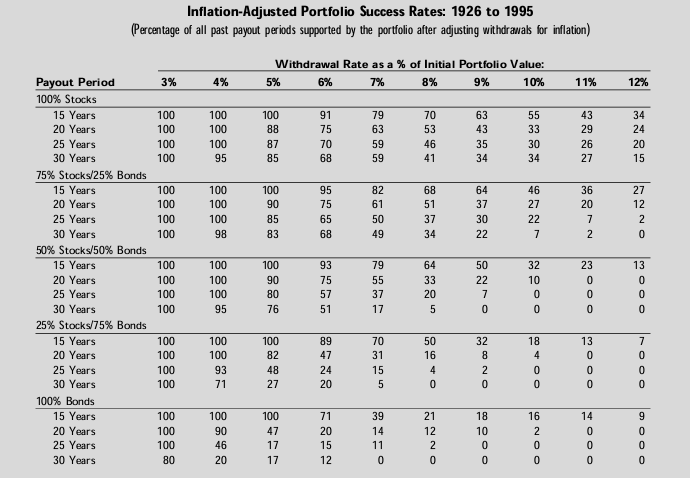

One thing that this chart doesn’t take into consideration is inflation. For example, an investor who plans to withdraw $70,000 per year from a $1 million portfolio of stocks and bonds (a 7% withdrawal rate) is likely to experience a decline in purchasing power due to inflation. If inflation averages 3% per year, the purchasing power of the $70,000 will be cut in half by the end of 25 years.

The Trinity Study also analyzed withdrawal rates with inflation-adjusted returns. Here are the results:

We can see that the results look slightly different, but a 4% withdrawal rate in a portfolio with 50% stocks and 50% bonds still has a 95% success rate. From this study, the authors concluded that 3-4% withdrawal rates are a good way to plan for anticipated portfolio draws.

Using the 4% rule, you can also anticipate the needed portfolio size for your own retirement. If you need $50,000 of income from your portfolio (with the rest coming from Social Security or a part-time job, for example), you will need roughly a $1.25 million portfolio.

When planning, some people prefer to be more conservative, so they use a 3% withdrawal rate instead of 4%. It’s better to plan for the worst than to be too aggressive with your projections. Additionally, early retirees who anticipate long payout periods (more than 30 years, for example) should plan on a lower withdrawal rate.

I hope you found this one useful.

See you next Saturday!

MC, CPA