I was scrolling on social media and saw a post about retirement accounts being “paper wealth” and people “waiting for permission” to access their money:

There are a lot of misconceptions around retirement accounts and how accessible they actually are.

So let me clarify a few things.

- You’ll likely live past 59½

Most people today are going to live well into their 60s, 70s and potentially 80s. Even if someone retires early, they still need assets in the future.

Ignoring retirement accounts for a 30 year old isn’t wise, because you will end up “wasting” 30-40 years of *tax advantaged* compounding. Even if you may not be able to access the growth of a Roth IRA account in your 30s, you can in your 60s. It’s not all or nothing.

In addition, you can rebalance strategically. You can always de-escalate your risk without having to pay expensive tax bills. You can sell freely in your Traditional IRA and buy any other funds that fit your strategy.

- SoSEPP

One of the most common arguments online is that retirement accounts are completely locked up until retirement age. That’s not true…

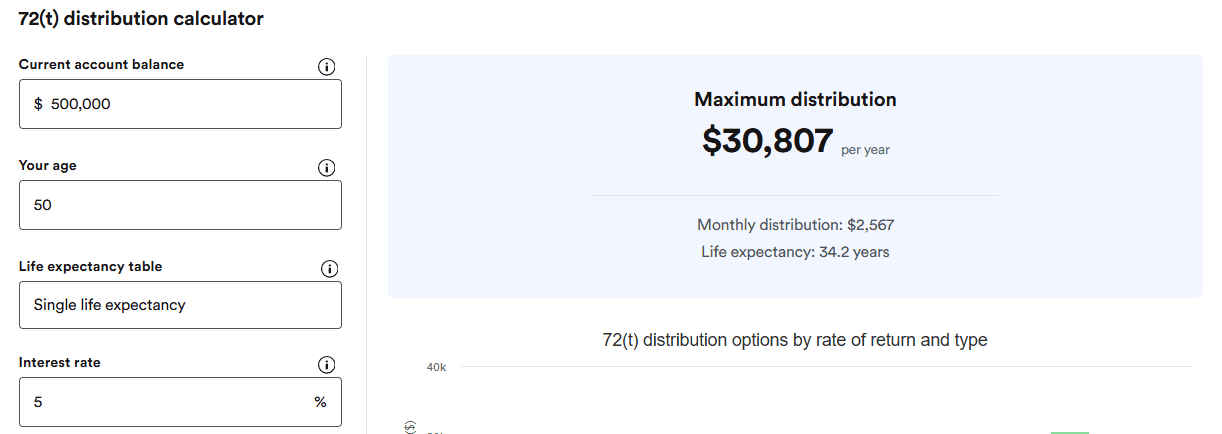

SEPP (Substantially Equal Periodic Payments), also known as 72(t), allows you to take penalty free withdrawals before age 59 1⁄2 from your retirement accounts if IRS rules are followed.

Using a 72(t) calculator, we can see that a $500,000 72(t) setup can result in a $30,807/year distribution, avoiding the 10% early withdrawal penalty:

So the idea that retirement accounts are inaccessible until you’re old is pretty outdated.

3. Rule of 55

Another thing people leave out is the Rule of 55.

If you leave your employer during or after the year you turn 55, you can often withdraw from that employer’s 401(k) without the normal 10% early withdrawal penalty.

So even before traditional retirement age, there are already mechanisms that allow earlier access, if needed.

4. Roth IRA withdrawals

Money you put into Roth IRA can also be withdrawn anytime tax and penalty free. Of course, you shouldn’t touch it, but it’s available.

In general though, Roth IRA is one of the most powerful accounts, because qualified withdrawals are tax free and there is no tax you have to pay on any dividends received.

As a wild example, according to ProPublica reporting sourced from IRS records, between 1999 and 2021 Peter Thiel grew his Roth IRA from $2,000 to more than $5 billion. Peter Thiel will turn 59½ on April 11, 2027, and will be able to withdraw billions of dollars tax free. Imagine if he said “I’m living life now!” and skipped it.

5. Employer match

Skipping a 401(k) match is one of the worst financial decisions someone can make.

If your employer offers a 2-3% match on your salary, you are effectively receiving an immediate return before your investments even grow. If you have a dollar for dollar match, it’s an instant 100% return on your contribution.

There are no other opportunities that are that attractive with this risk profile.

In addition, you can literally withdraw all the contributions (including employer match), pay the tax, pay the 10% penalty, and you will likely come out ahead as if someone had only contributed to a brokerage account and didn’t receive the employer match.

6. Tax benefits

Inside a retirement account:

- Dividends can compound without tax hits

- You can rebalance investments without triggering taxable events

That matters over long periods of time. Now compare that to a taxable brokerage account:

- Dividends generally create a yearly tax drag

- Selling appreciated investments can trigger capital gains taxes

- Rebalancing can create taxable events

Inside retirement accounts, compounding becomes much more efficient.

You are also able to arbitrage taxes on your contributions. For example, you can contribute at 22-24% marginal tax rates, receive a tax deferral, and withdraw at 10-12% marginal tax rates.

In some states, you can receive tax benefits when contributing and later pay little to no state tax on retirement withdrawals. That’s a massive long term advantage most people have no clue about.

7. Roth conversion ladders

Roth conversion ladders are also another common strategy used by early retirees.

The basic idea is:

- Move money gradually from a Traditional IRA or 401(k) into a Roth IRA

- Pay taxes on the conversion amount

- Wait 5 years

- Withdraw converted funds penalty free

So there are ways you can access your money.

The main point is that it’s not all or nothing. You should use brokerage account, Roth IRA, and 401(k). They are all tools designed to provide flexibility during retirement.

I’m glad she marked it as an “unpopular opinion” at least…

Chat next week.

MC, CPA