JP Morgan published their 56 page 2025 retirement guide, and I wanted to share some insightful data points from it.

Let’s dive right in!

How long will I live?

First, if you are 65, you have a pretty high chance of living till 85. So, our retirement plan needs to take that into consideration:

How will I fund my retirement?

Well, depending on your household income, a majority will come from:

- Decrease in spending and taxes

- Social Security benefits

- Savings and employer plans (like pension/401ks)

Let’s say your pre-retirement income is $100k. In order to maintain an equivalent lifestyle in retirement:

- You might need about 76% of that in retirement → $76k/year (due to lower taxes/expenses)

- ~$33K will come from Social Security

- ~ $43K/year that you need to provide yourself through savings, investments, and employer plans

- ~$33K will come from Social Security

How much should I have saved up?

Here’s a rough analysis of how much you should have saved up.

Example: For a 40 year old with a household income of $100,000, your current retirement savings should be $200,000.

Again, these are just rough assumptions based on a conservative risk profile, inflation, and retirement age.

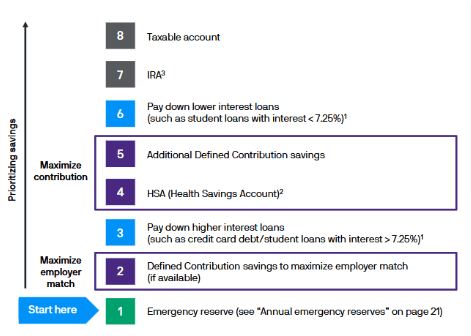

How do I get started?

One thing I would add to the above chart is between 4 and 5 – see if your employer offers an Employee Stock Purchase Plan (ESPP). Depending on the discount, it could be an easy 10–15% return if you sell immediately.

Also, before doing a taxable account on step 8, see if your employer offers a Mega Backdoor Roth, as it could be more beneficial than a taxable account in many cases.

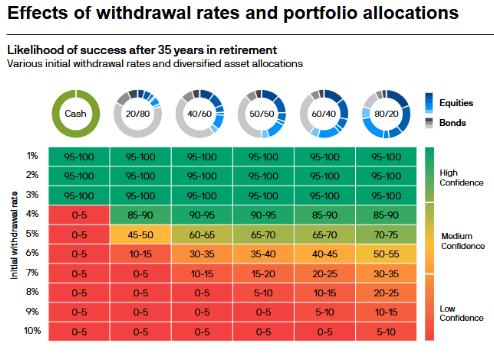

Withdrawal rates

You may have heard of the 4% rule, which is typically used as a baseline for the maximum amount you should pull from your portfolio at retirement.

The chart below shows a 35-year timeframe with different asset allocations and likelihoods of success:

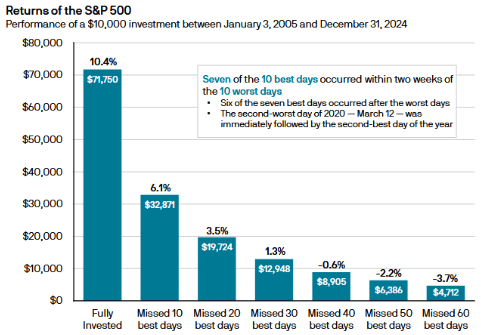

Another important chart:

7/10 best days offered within 2 weeks of the 10 worst days. Stay invested!

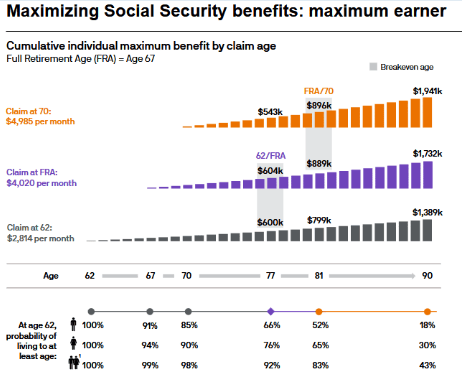

Social Security benefits:

You could delay receiving Social Security benefits for an increased payout. The chart below shows the difference in benefits:

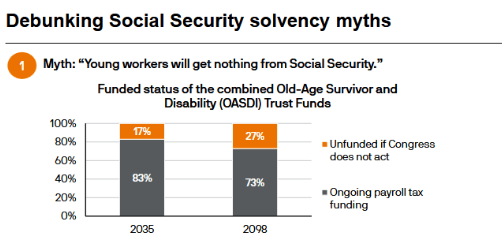

Will Social Security even exist by the time I retire?

I like the below chart. It shows that ongoing payroll tax funding will still support a majority of benefits for years to come, but could decrease without support from Congress.

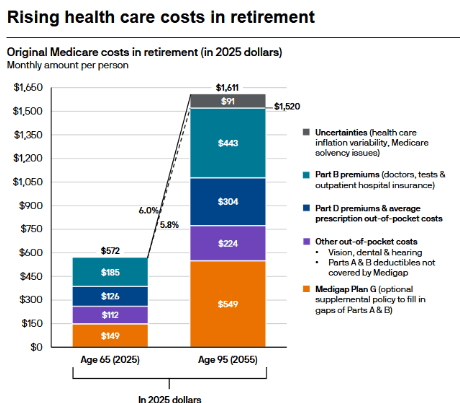

Healthcare

A final note – health care will go up as you age, so take that into consideration.

Overall, start planning for your retirement today.

It doesn’t matter if you are 25 or 45. Put a plan together and stick to it. Your future self will thank you.