There are many ways to withdraw from your 401k or IRA accounts without a penalty.

However, most of the things come with some strings attached.

For example, here are some distributions that are not subject to the 10% penalty, from the IRS list:

- After participant/IRA owner reaches age 59½

- Distributions up to $5,000 per child for qualified birth or adoption expenses

- Up to $22,000 to qualified individuals who sustain an economic loss in a federally declared disaster

- Victim of domestic abuse by a spouse or domestic partner, up to the lesser of $10,000 or 50% of account

- Qualified first-time homebuyers, up to $10,000 (IRA only)

- Unreimbursed medical expenses (>7.5% AGI)

- Health insurance premiums paid while unemployed (IRA only)

- Qualified higher education expenses (IRA only)

But, what if we wanted to withdraw to pay for some living expenses? Or take care of our family?

2 weeks ago, I shared a newsletter about a 72(t) plan that you can create to start withdrawing earlier by establishing series of substantially equal periodic payments. But, there is also a Rule of 55.

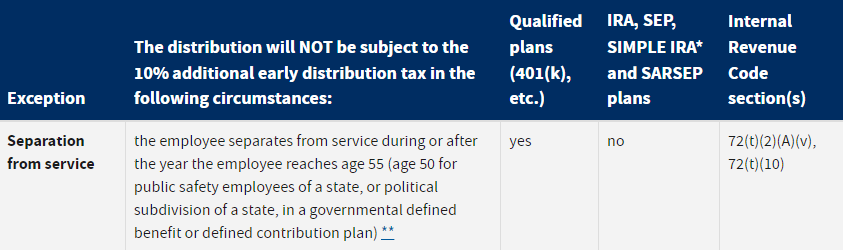

Rule of 55

This rule is more flexible than a 72(t) plan and much simpler to execute.

It applies to individuals between 54 and 58 years old and allows you to withdraw from a 401(k), 403(a), or 403(b) without the 10% penalty:

In simple terms, if you quit your job in the calendar year when you turn 55 (or 50 for qualified public safety employees) or older, you can start withdrawing from your retirement plan. The reason for separation does not matter. However, you can’t separate from service before that year, wait until you are age 55 (or age 50 for QPSE), and then take a distribution.

For example, if you are 54 years old, quit your job in May, and turn 55 in December, you are eligible to withdraw from your 401k without a 10% penalty.

However, if you quit your job at 52, you cannot start withdrawing at 55 without incurring the 10% penalty, since you separated from service before reaching age 55.

The separation from service exception only applies to the qualified plan (401k, 403b, etc.) you have with that employer, not to an IRA or SEP.

However, one thing you can do is to rollover your IRA or SEP plan into the 401(k) before you quit. That way, the entire balance will be eligible for withdrawal.

So, if you have $50,000 in an IRA, you can roll it into a 401(k) without any penalties and withdraw it penalty-free.

You can also combine this strategy with 72(t) to strategically start withdrawing much earlier than at age 59 ½.

Qualified Public Safety Employees

If you are a qualified public safety employee, you are eligible to start withdrawing after the year in which you turned 50. The definition of qualified public safety employees includes:

- Any employee of a State who provides police protection, firefighting services, emergency medical services, or services as a corrections officer

- Federal law enforcement officers,

- Federal customs and border protection officers,

- Federal firefighters,

- Air traffic controllers,

- Nuclear materials couriers,

- Members of the United States Capitol Police,

- Members of the Supreme Court Police, and

- Diplomatic security special agents of the United States Department of State.

Final thought

In the end, there are many strategies you can utilize to avoid paying taxes or penalties. Remember, retirement is just a number in your investments. My goal with these newsletters is to show you strategies for paying less tax, improving your finances, and achieving freedom.

See you next Saturday