In this newsletter, I want to discuss efficient tax decumulation strategies. This subject is not the easiest, as there are a lot of things you have to be aware of, but I will try to make it understandable.

When investing, we generally have three main account types:

- Tax-deferred accounts (TDA) – Traditional 401(k)/IRA

- Tax-exempt accounts (TEA) – Roth IRA, Roth 401(k)

- Taxable accounts

Each of these accounts has different tax implications, so it’s important to be strategic later in life when it comes to withdrawals. Our strategy should aim to minimize taxes over the long term and maximize the longevity of the portfolio.

So, how do you withdraw efficiently?

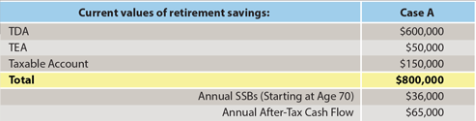

I wanted to bring in some examples from the research paper “A Comparison of the Tax Efficiency of Decumulation Strategies.” Here is one real-world example:

And assume the following fact pattern:

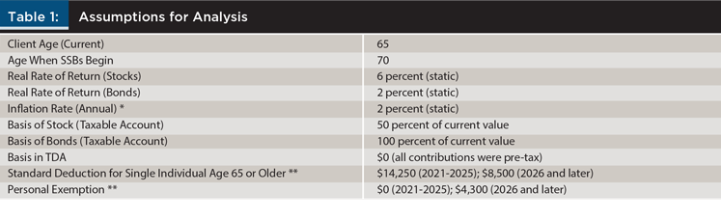

First, before Social Security Benefits (SSB) begin, we have to liquidate the tax-deferred and taxable accounts in an efficient manner. This will help us prevent a huge tax increase later on with Required Minimum Distributions (RMDs) and SSBs.

A few reminders:

- Taxable accounts can have a 0% tax rate depending on your taxable income.

- The standard deduction for single filing status and age 65 or older is $16,550, which means we can withdraw that amount from a TDA and pay 0% in taxes.

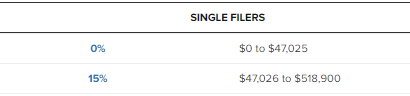

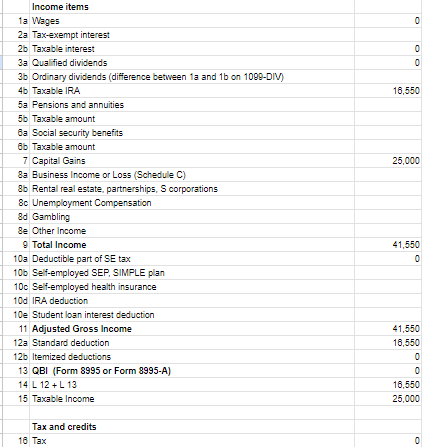

First, you can pull $16,550 (up to the standard deduction) from a TDA and pay 0% in tax. Then, you can withdraw $50,000 from a taxable account, of which $25,000 would be taxable (since 50% is the basis).

However, since your taxable income would be below $47,025, you would pay 0% in tax. Your total cash withdrawal is $65,550, which meets the annual cash flow needed, and you also paid 0% tax on it.

Here is how the tax return would look like:

P.S. I’m creating an entire Tax Return Excel spreadsheet that will help you run many of these projections. Click here to join the waitlist.

However, as part of the withdrawal strategy, we want to minimize the future tax impact before SSB and RMDs kick in. This is the perfect time for Roth conversions.

When you originally contributed to a 401(k), you received a tax deduction, ideally at 24% or higher. When you start withdrawing, you pay taxes, which is why it’s called tax-deferred. The goal would be to withdraw these deductions at the 10-12% tax bracket, thereby creating a 12%+ tax savings spread.

So now, in our scenario, we still have roughly $22,000 of taxable income before our capital gains would be taxed at 15%. We would withdraw these $22,000 from a TDA and convert it to a TEA.

So in total we withdrew $80,000 of cash and only ended up paying ~$2,408 in federal taxes. Not bad.

In addition, this client was able to stay below the IRMAA threshold, avoiding an increase in their Medicare premiums, which is also an important aspect to consider. In higher income scenarios, you would also need to consider the impact of the 3.8% Net Investment Income Tax, but this doesn’t apply in this case.

In this scenario, we would continue this strategy for the next 5 years before SSB begins. The goal would be to strategically live off taxable accounts and TDAs, converting to TEAs, and reducing the amount in TDAs to prevent future RMDs.

After SSBs start, TDA withdrawals should be taken up to the 10-12% tax brackets, with additional income supplied from the TEA.

Research showed that this method would actually produce the highest portfolio longevity of 32.83 years:

By the end of this newsletter, some of you might think, “Well, I’m only retiring in 30 years; I have time!” However, it’s important to start thinking and be aware of how different things are taxed so you can plan your contributions to various account types.

I hope you learned something new today.

See you next week.

MC