Tax gain harvesting is the process of selling your appreciated securities tax-free.

This concept applies only to brokerage accounts and does not apply to any retirement accounts.

IRS Topic No. 409 states that a long-term capital gains rate of 0% applies if:

- Your taxable income is less than or equal to $47,025 (for single tax filing)

- Your taxable income is less than or equal to $94,050 (for married filing jointly)

A reminder: the long-term capital gains rate applies to stocks/ETFs held for more than 1 year. These preferential rates do not apply if you held a stock for less than a year.

Application

Say you purchased 50 Apple shares for $50. In the tax world, $50 is the cost basis. Your total purchase is $2,500

If the price of Apple is now $150 and you decide to sell, your proceeds (total sales price) will be $150*50 or $7,500. Since your cost was $2,500, the realized gain will be only $5,000, and this is the taxable amount.

Great investment!

Not so fast, IRS!

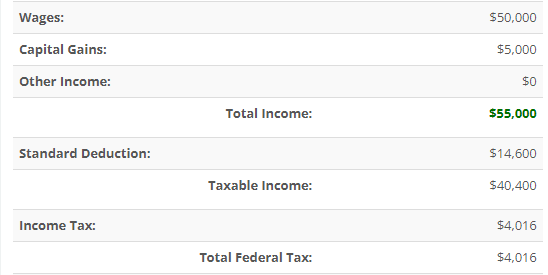

If you have a $50,000 salary, and sold $7,500 of stocks (with a taxable gain of $5,000) your total gross income is $55,000.

You will pay $4,016 in federal taxes:

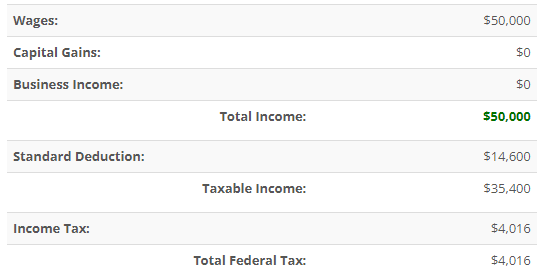

What would have happened if you didn’t have that $5,000 of capital gains from the Apple sale?

Your tax would still be $4,016!

Why?

Because $50,000 of wages minus $14,600 of standard deduction = $35,400 of taxable income.

If you add $5,000 to it, you will have $40,400 of taxable income, which is below the $47,000 threshold for 0% tax for capital gains tax. So you basically generated $5,000 tax free. The amounts double if you are filing as married filing jointly (MFJ).

Additional tax planning opportunity

One of the tax planning opportunities that exists is to pay $0 in taxes on your capital gains, use the proceeds you just generated, and buy back that same stock (or different).

What happens in this case is that you are increasing the cost basis of your stocks for future sales.

Example – you purchased $2,500 of stocks, sold them for $7,500, realized $0 in taxes.

Now you can use $7,500 and buy back that same stock. Your cost basis becomes $7,500, and in the future when you have to sell the stocks, you will use $7,500 as your cost. This only works as long as you pay $0 in taxes when you buy it back.

I understand that a lot of people earn more than ~$50,000 (~$100,000 MFJ), but this strategy can be especially impactful during retirement, getting your Master’s degree or taking a break from work, since your income will be lower. You can also combine it with the Roth conversions!

See you next Saturday.