Welcome to The Crunch‘s first newsletter issue! My goal with these is to provide as much valuable insight as possible about the world of personal finance.

We’ve all heard about Roth retirement accounts and their benefits. The main advantage often discussed is the tax free withdrawal during retirement. But, there are many other benefits that people may not think about:

1. Tax rate protection

One thing we have no control over is tax rates..

Did you know that in the 1980s, the highest tax rate was 50%? In the 1970s, it was almost 70%, and in the 60s, it was as high as 91%! Currently, we have historically low tax rates. The government deficit in 2023 was $1.7 trillion, and raising taxes is one way to decrease that deficit.

2. Social security tax

If we live long enough, we might receive some Social Security income.

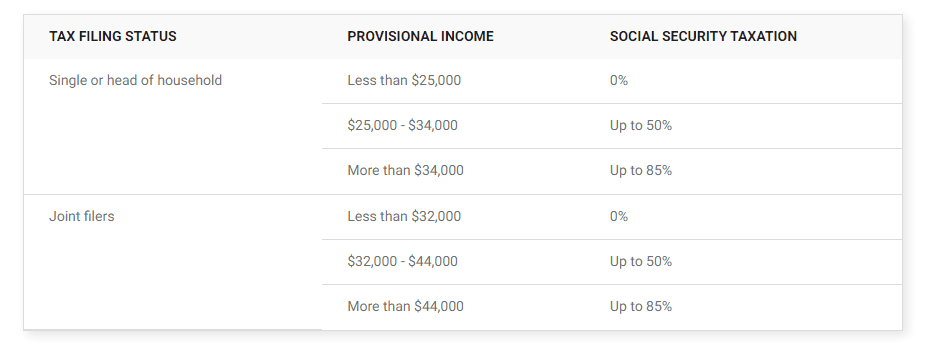

Depending on whether you are single or married, there is a limit on the amount of provisional income you can have during retirement before your Social Security gets taxed.

So, if your provisional income is less than $25,000 (single), 100% of your Social Security is tax free. Provisional income generally includes traditional IRAs, 401(k)s, income from employment, capital gains, rental income, and half of your Social Security income.

However, Roth accounts are not in that category. This means that Roth IRA or Roth 401(k) withdrawals do not count toward provisional income.

3. Medicare premiums

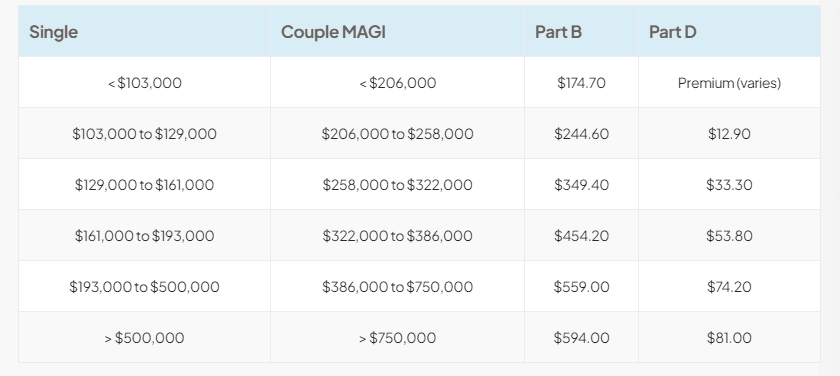

This tax, or extra premium, is based on your income. If you are single and your income exceeds $103,000, you will have to pay increased premiums.

The higher your income, the more you have to pay. Your premiums can increase almost 3x if you make a significant amount of income.

But, tax free withdrawals do not count toward these thresholds.

4. Required minimum distributions (RMDs)

Once you turn 72, you are required to withdraw a percentage of all your tax deferred investments (traditional IRA/401(k)) based on your age and pay taxes on them.

By using Roth IRA and Roth 401(k), you don’t have to withdraw anything. You can time your withdrawals strategically.

5. Early withdrawal penalty

When you withdraw from a 401(k)/traditional IRA early, you have to pay a 10% penalty along with taxes on it.

For Roth IRA/401(k), you can always withdraw up to your contributions at any time with no penalty.

If you can’t contribute to a Roth IRA account due to the income limitation, you can use the Backdoor Roth strategy to contribute. It’s an easy way to bypass the restriction.

Actionable tip:

Start taking Roth IRA/Roth 401(k) more seriously. Don’t just focus on traditional 401(k)s/IRAs. Having tax free withdrawals will provide you with many options regarding flexibility and control of your taxes in the future.