We’ve all heard about using a High Yield Savings Account (HYSA) to park our money for emergency funds, down payments, etc.

But there’s another option that some people aren’t as familiar with—Treasury Bills.

Treasury Bills (T-Bills) are short-term instruments issued and backed by the U.S. Treasury. They are available in terms of 4, 8, 13, 17, 26, and 52 weeks.

T-Bills are issued at a discount to their face value and reach par value (full value) at maturity. The difference between the discounted purchase price and the par value is the interest you’ve earned.

To calculate the purchase price for a specific discount rate, use the following formula:

Price = Face value × (1 – (discount rate × time) / 360)

Example: A $10,000 4-week T-Bill sells at auction for a discount rate of 5.145%.

Price = 10,000 × (1 – (0.05145 × 28) / 360) = $9,959.98

According to the formula, the T-Bill sells for $9,959.98, giving you a discount of $40. After 4 weeks, when you receive $10,000, you’ve effectively earned $40 in “interest.”

T-Bills can be purchased from banks, brokers, and directly from the U.S. Treasury through TreasuryDirect.

Taxation

The interest income from a Treasury bill is exempt from state and local income tax.

This is a significant advantage over a HYSA, which is subject to both state and local taxes.

For example, if you are in a 5% state tax bracket and a 20% federal tax bracket, and your HYSA has a 5% yield, your after-tax yield would be 3.75%.

With a 5% T-bill, your after-tax yield would be 4%, since it’s not subject to state taxes.

This is especially beneficial for people in high-tax states like CA, NY, NJ and others.

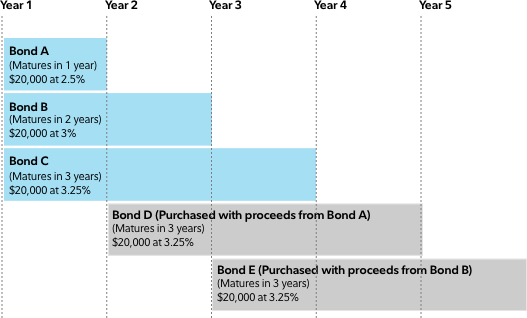

T-Bill Ladder

Some people use the “T-Bill Ladder strategy”, where they buy T-bills of varying lengths to maximize liquidity.

Here’s an easy visualization of the concept:

One common approach is the 4-rung, 4-week ladder.

For example, if you have $10,000 to allocate to your emergency savings, you would start by using $2,500 to buy a 4-week T-bill. The next week, you would buy another $2,500 4-week T-bill, and continue doing this for 4 weeks ($10,000 ÷ 4 = $2,500 per week).

What this strategy accomplishes is that after the initial 4 week period, you’ll have a T-bill maturing and paying you interest every single week. This way, you won’t have to sell your T-bills before maturity if you need to access your funds early.

Various brokers, like Fidelity, offer an “auto-roll” service that automatically reinvests your funds, reducing the need for constant manual purchasing.

T-Bill ETFs

If you don’t want to buy T-bills directly, you can purchase an ETF that invests in Treasury Bills.

Of course, with convenience comes a small expense, as these funds charge management fees.

Here are a few examples:

The expense ratio is 0.1356% and the 30 day SEC yield is 5.18% (after expenses)

The expense ratio is 0.09% and the 30 day SEC yield is 5.24% (after expenses)

Keep in mind, though, that lower interest rates will impact the yield of Treasury bills. Holding T-bills is not a good long-term investment strategy and should only be used for your emergency savings or future cash needs.