If you have a Money Market Fund (i.e., VUSXX, VMFXX), Treasury fund (SGOV), or any other Treasury ETF, you need to know how to report it on your taxes correctly. If you don’t, you are overpaying on your state taxes.

How and why?

Well, these funds hold U.S. Treasury Bills. Treasuries are exempt from state and local taxes. This only matters if you hold these funds in a taxable brokerage account, which most people do.

The broker sends you a 1099-DIV form, but it’s your responsibility to figure out how to report it on your taxes correctly.

(By the way, bad tax preparers/CPAs can miss this sometimes.)

The 1099-DIV doesn’t break out how much of the dividend was allocated to Treasuries. The software also wouldn’t know how much based on the 1099-DIV. This means that you have to figure out how to report it (or ensure your CPA does it correctly).

Now, the 1099-DIV will have a breakdown of every single stock/ETF you have, but you have to find out the percentage of a fund that holds Treasuries.

Let me give you an actual example. I will use the 2023 tax year, as 2024 is not finalized yet.

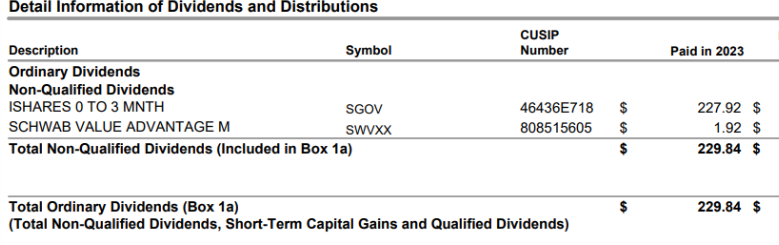

Say, in 2023, you received $229.84 of dividends from two funds. So, the 1099-DIV will have these amounts in Box 1:

Then, if you scroll down, you will see a “Detail Information” of your dividends:

We can see that $227.92 came from SGOV (Treasury 0-3 Month ETF) and $1.92 from SWVXX (Schwab Money Market Fund).

The entire $229.84 will be taxed at the federal level, but how do we figure out what’s taxed at the state level?

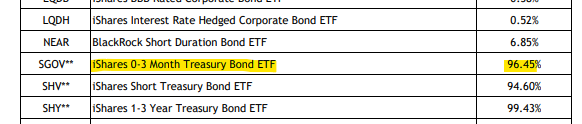

During the end of the year, the fund manager (i.e., iShares for SGOV) will post a “US government source income information” on their Tax page.

We can see that 96.45% of SGOV’s holdings for the 2023 tax year were income derived from the U.S. government and, therefore, are not taxable at the state level.

So, we would take $227.92 * 0.9645 = $219.83. Of the total, $219.83 is derived from U.S. obligations, and you would only pay state taxes on the remaining ~$8.

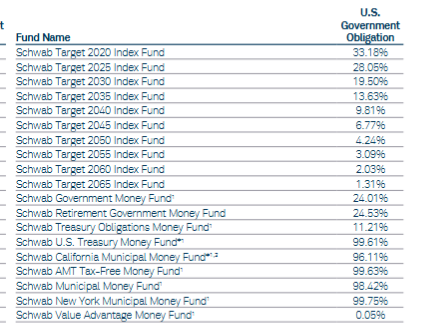

The second fund, Schwab Value Advantage Money Fund, had $1.92 of dividends, and only 0.05% is not taxable at the state level:

However, it’s important to note that some states say, “hey, if less than 50% of the fund is from the U.S. government (like Treasury Bills), you can treat it as 0%.”

For example, California, Connecticut, and New York are some of these states. So, if the fund has only 0.05% coming from the Treasury, you shouldn’t even calculate the exempt amount for these states.

SGOV, having 96%, is more than 50%, therefore qualifying for the state tax exemption.

Now, if you buy Treasuries directly from TreasuryDirect, they will send you a 1099-INT, and you can just enter that information directly into the tax software. No extra calculations are needed.

So, how do you report that dividend interest calculation?

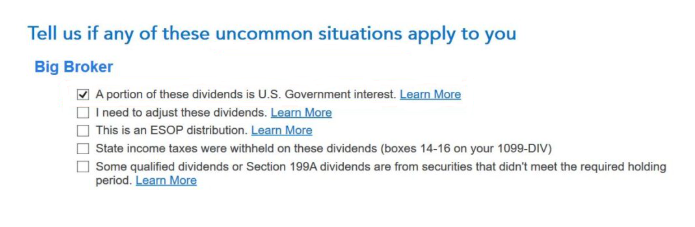

In TurboTax, after entering the 1099-DIV, it will ask:

So, you would just check off the first one and enter the amount from Treasuries ($219.83 in our example).

Some software (like H&R Block) might ask for the percentage of dividends that are state tax exempt. However, this is a bit tricky because you might receive other dividends in your brokerage account. In that case, calculate the amount from the Treasury, say $219, and divide it by your total dividend amount, say $1,000, and you would enter 21.90%.

If you have someone do your taxes and you have some of these Money Market Funds or other Treasury ETFs, double-check your state tax return and see the amounts reported. This will save you some $$.

If you live in a no tax state, this would not apply to you, but still good to know in case you move!

I hope you found this one valuable.

See you next Saturday.

MC, CPA