A week ago a reader asked, “As someone about to enter the workforce after college, what do you believe are the best 3–4 things to do financially in that first year?”

I love this question because I believe a few right moves will help set you up for success.

Here are 7 things that I would focus on (assuming you already have a job lined up):

- Budget & tracking

I saw so many of my friends entering the workforce and spending all of their money. This happens very often as people just start earning full-time wages.

I suggest setting up a Needs/Wants/Savings budget and tracking as you go along. Ideally, the savings percentage should be at least 15%.

Having a clear understanding of exactly where your money is going every single month is crucial.

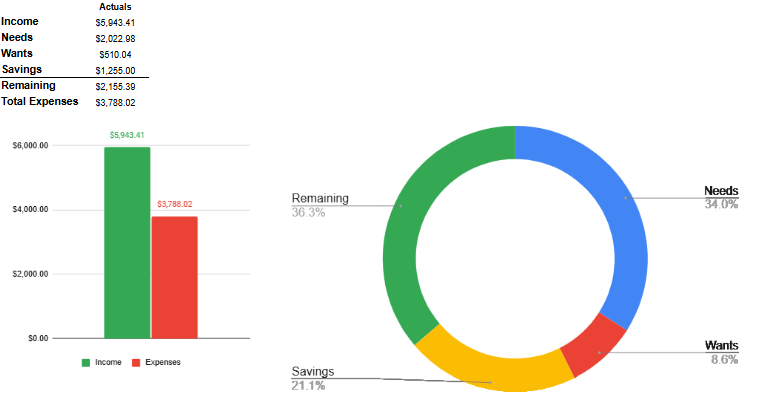

I personally have a spreadsheet to track money coming in:

You could also use some budgeting apps, but I’m not the biggest fan of those. I like to control what I see on my spreadsheet.

If you want the spreadsheet, just reply to this email and tell me you want it. I will send it to you.

- Emergency Fund

There will always be something unexpected that comes up. Start saving your money.

Typically, save 3–6 months of your monthly expenses. This could be lower if you don’t have a car payment, live with your parents, etc., but it is a good start.

Make sure to use a high-yield savings account (HYSA) or a money market fund (MMF) for this account. Either of these should get you at least 4% yield. I also wrote a newsletter covering HYSA vs MMF in depth.

- Retirement plan up to the match.

Sign up for your workforce retirement plan ASAP. Pretend that money is not even there.

For example, many plans offer a 3% match on your 3% contributions. This is a great way to start building your financial foundation. Receiving a match is a 100% return on your money. However, keep in mind vesting rules related to keeping that match.

If you are also earning, say, $50,000/yr, you should also select the Roth version of the 401(k) since you will be in a 12% federal tax bracket. You could switch to the Traditional version as you start earning more money. I discussed Roth vs. Traditional in my other newsletter issue.

- Credit Card

Apply for a credit card to build credit if you don’t have one already. But make sure you pay the balance IN FULL, on time, every month. I suggest a simple credit card setup:

- Citi Double Cash Card for 2% cash back.

- Citi Custom Cash 5% cash back on groceries (up to $500/mo).

If you are a big overspender and your bank account goes negative every month, you should stay away from credit cards in general, until you build the financial habits.

- Debt.

Pay off any debt with interest rates ~5% or higher. If you have any student loans (5%+) or credit cards (~25%), get rid of them ASAP. That is a guaranteed, tax-free return on your money.

If you have a large private student loan balance, try to refinance it if possible.

- Max out HSA.

HSA account offers triple tax benefits:

- Tax deduction.

- Tax-free growth.

- Tax-free withdrawal for medical expenses

It’s basically a Roth IRA on steroids! Since you are young and ideally in the best health shape you would be, a high-deductible health plan could be a great choice. This would allow you to contribute to an HSA.

- Human Capital.

At the end of the day, you have to remember that you are your greatest asset. You have to do everything you can to continue growing professionally.

Figure out what you want to do. Work hard. Get certifications.

When I got my CPA and switched jobs, I increased my salary by 50%. Imagine how much easier investing, paying off debt, or living is after a 50% raise.

It’s a no brainer but frequently missed by young people.

If you have any suggestions on the content you want to see, feel free to reply to this email. I read all the emails.

See you next week.

MC, CPA