My coworker recently retired. He is 50 years old and has been with the company for over 25 years.

The company offers a decent 401(k) match (100% match on 6% of your salary) along with other great benefits.

In his case, how can he generate income? How can you retire early if most of your assets are in retirement plans?

Most tax-advantaged accounts have restrictions on withdrawals, but there are a few strategies that many people don’t know of:

Running the numbers

There are a lot of estimations on the safe withdrawal rate.

According to FireCalc, a 3.5% withdrawal rate (plus inflation adjustment) has a success rate of 100% for 30 years. While it’s not a perfect measure, it’s something that we can use as a baseline calculation.

So, for a $1.5M portfolio, you can safely withdraw ~$52,500/yr.

Say my coworker was able to get a $1.5M portfolio with the following split: $1M in a traditional 401(k), $300,000 in a taxable brokerage, and $200,000 in a Roth IRA.

What’s the withdrawal strategy?

- SEPP

First, I would probably roll over the 401(k) balance into 2 separate rollover IRAs (split 60%-40%).

This move would allow you to set up the “Substantially Equal Periodic Payments” (also called the 72(t) strategy) and avoid the 10% penalty on withdrawals. This plan would be established only on the 60% IRA.

There are three different methods (RMD method, fixed amortization, or annuitization) for calculating the amounts you can withdraw. I discussed this strategy more in-depth in my prior newsletter. Using a 72(t) calculator, we can see that a $600,000 72(t) setup can result in a $36,969/year distribution, avoiding the 10% early withdrawal penalty.

- Brokerage account

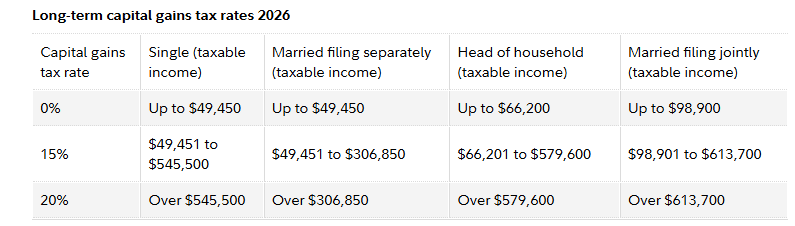

With $300,000 in a brokerage account (say invested in $VTI), we are looking at ~$3,720 in dividends (95% of them will be qualified). Since our taxable income will be below $49.450, most will be taxed at a 0% rate.

In addition, say that the $300,000 portfolio had 75% of it in capital gains and 25% in basis.

We can sell an additional $10,500 of VTI per year and have only $7,875 of long-term capital gains, taxed again at a 0% rate.

So far, we’ve pulled $36,969 + $10,500 + $3,720 = $54,189. This would put us right at around a 3.5% safe withdrawal rate.

- Roth IRA Withdrawals

In addition, while not needed in this case, you can also minimize your 72(t) withdrawal amount (by rolling over less into the account to be subject to the rules) by withdrawing your contributions from the Roth IRA.

Contributions can always be withdrawn penalty-free at any time (different rules apply to earnings/conversions, though).

Taxes

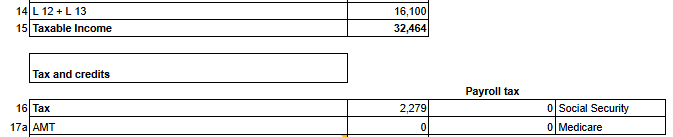

From the tax standpoint, he’ll pay ~$2,279 of federal tax in 2026:

(Assuming single, no kids)

This is ~7% effective tax rate.

Because the tax rate is very low, it may make sense to withdraw less from the brokerage account, and increase the 72(t) withdrawal. This can help prevent future RMDs, and can help with step-up in basis for his heirs.

Depending on the state, you might also pay no state taxes, either on full income, or partially on capital gains and/or retirement income.

What about health insurance?

One of the benefits of controlling your portfolio withdrawals is that you can predictably estimate your income. While the enhanced premium tax credit expired as of 2025, because of the lower income you may be able to qualify for subsidies on the state level.

Social Security Benefits

Before Social Security benefits (SSB) kick in, you can also do Roth conversions to further reduce the size of the 401(k) (and lower your future RMDs) and move more money into a Roth IRA.

Withdrawals from a Roth IRA don’t count toward provisional income for the SSB tax calculation, allowing you to minimize your tax liability.

In addition, controlling your income will allow you to be below the IRMAA (Income-Related Monthly Adjustment Amount) threshold. This surcharge increases Medicare Part B and Part D premiums for higher incomes but doesn’t apply to income below ~$100,000.