In previous newsletter issues, I’ve discussed Roth IRAs, their benefits, and how to open one. But what about withdrawing money from Roth IRAs?

It’s actually not that simple, as there are multiple ways to get your money into a Roth IRA (direct contribution, rollover, etc.), and they are all treated differently when withdrawing.

To preface, all your contributions (money you put in) can always be withdrawn tax-free and penalty-free at ANY time.

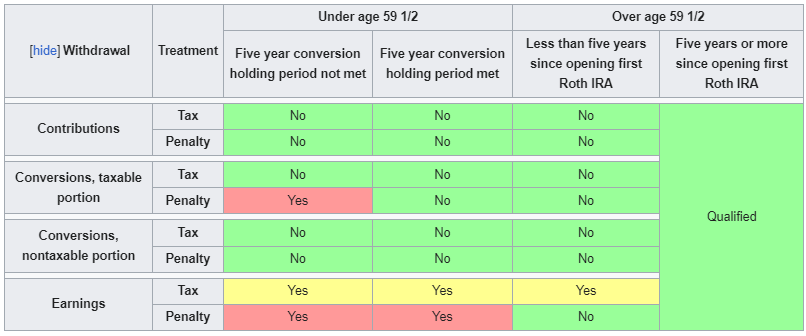

There are basically 4 distinct scenarios that will determine whether you need to pay any penalty (10%) and tax:

- You are over 59 ½ years old and 5 years or more elapsed since opening your first Roth IRA

If this is the case, ALL your money, regardless of where it came from (direct contribution to Roth IRA, Roth 401k conversion, Backdoor Roth conversion, Mega Backdoor Roth conversion, earnings), can be withdrawn tax-free and penalty-free from a Roth IRA.

- You are over 59 ½ years and and 5 years have not elapsed since opening your first Roth IRA

If this is the case, you can withdraw all your direct contributions and conversions (i.e. Backdoor Roth) tax and penalty free. Earnings, or growth, associated with your contributions or conversions will be subject to tax, but without a 10% penalty.

For example, say you opened a Roth IRA at the age of 60. You contributed $6,000 to the account. Now, the account has grown to $7,000. The $6,000 can be withdrawn tax and penalty free, and $1,000 of earnings will be subject to tax, but no penalty.

- You are under 59 ½ years and 5 year conversion holding period was met

If this is the case, you can withdraw all your direct contributions and conversions (e.g., Backdoor Roth) tax and penalty-free. Earnings (i.e., growth) will be subject to tax AND a 10% penalty.

Example – you are 40 years old. You contributed $6,000 directly to the Roth IRA account. For the next year, you used a Backdoor Roth IRA method to contribute to Roth IRA by transferring $5,005 from Trad IRA to Roth IRA ($5 were earnings that were taxed, $5,000 non-deductible contribution). Now 5 years later, the Roth IRA balance is $20,000. You can withdraw the $6,000 tax and penalty free. Since 5 years passed, you can also withdraw your conversion (including $5 of earnings) tax and penalty free. The remaining $8,995 you withdraw will be subject to tax and 10% penalty.

- You are under 59 ½ years and 5 year conversion holding was not met (for Backdoor Roth or Roth conversions)

If this is the case, you can withdraw all your direct contributions tax and penalty-free. The taxable portion of the conversion will be subject to a 10% penalty. Earnings (i.e., growth) will be subject to tax AND a 10% penalty.

Example – you are 40 years old. You contributed $6,000 directly to the Roth IRA account. Over the next few years, you used a Backdoor Roth IRA method to contribute to the Roth IRA by transferring $5,005 from a Traditional IRA to the Roth IRA ($5 were earnings that were taxed, and $5,000 was a non-deductible contribution). Now, 2 years later, the Roth IRA balance is $20,000. You can withdraw the $6,000 tax and penalty-free (direct contribution). Since 5 years have not passed, you will be subject to a 10% penalty on the $5, but you can withdraw your $5,000 contribution tax and penalty-free. The remaining $8,995 you withdraw will be subject to tax and a 10% penalty.

A chart will help you visualize these scenarios:

There are also ordering rules for withdrawals:

First, your withdrawals count from your contributions, then (oldest to newest) conversions (taxable portion), then conversions (non-taxable), then earnings.

In summary, if you don’t have any conversions (like using Backdoor Roth or IRA -> Roth IRA), you don’t have to worry about the conversion portion (row 2 and 3).

Contributions can always be withdrawn tax-free and penalty-free. Earnings depend on whether you are over 59 ½ and age of Roth IRA account. Additionally, IRS allows a few exceptions from the 10% penalty (not taxes) on the earnings:

- You use the withdrawal (up to a $10,000 lifetime maximum) to pay for a first-time home purchase.

- You use the withdrawal to pay for qualified education expenses.

- You use the withdrawal for certain emergency expenses.

- You use the withdrawal for qualified expenses related to a birth or adoption.

- You use the withdrawal to pay for unreimbursed medical expenses or health insurance if you’re unemployed.

- You are a survivor of domestic abuse.

- The distribution is made in connection with a federally qualified disaster.

- The distribution is made due to an IRS levy.

- The distribution is made in substantially equal periodic payments.

It’s important to keep ALL records related to your IRAs. Have a spreadsheet that tracks your contributions, withdrawals, dates, any conversions, and all your forms that you receive related to Roth IRA (1099-R, 5498). It will help you in case of an audit or for tracking purposes.

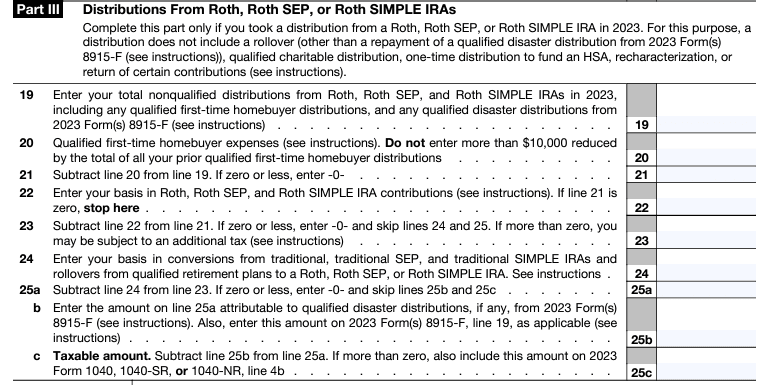

All Roth IRA withdrawals are reported on the IRS form 8606 part III:

Every week I try my best to share the most insightful personal finance content at no cost. It would mean the world to me if you can share my newsletter with friends or family.

Any questions? Reply back.

MC, CPA