Roth IRA is an extremely powerful account. It allows for tax-free withdrawal during retirement. I talked about all the benefits in the other newsletter issue.

Roth IRA also has income limits.

For 2024, if you are filing your taxes as single and make less than $146,000 ($230,000 if married) of adjusted gross income, you can contribute a maximum amount of $7,000. If you make between $146,000 ($230,000) and $161,000 ($240,000), the contribution is reduced.

If you make $161,000 ($240,000 if married) or more, no contribution is allowed, but there is a loophole..

Backdoor Roth

Backdoor Roth is a strategy that allows high-income earners to contribute to a Roth IRA through a rollover.

Here is a step-by-step guide:

1. Open a Traditional IRA account

Register for a Traditional IRA account or use the one you already have.

2. Contribute to a Traditional IRA (limit $7,000 in 2024)

Instead of contributing to the Roth IRA, you will contribute to a Traditional IRA account.

Importantly, you must have a $0 balance in either a Traditional IRA, Rollover IRA, or SEP IRA by the end of the year in which you are doing the Backdoor Roth. If you have a balance in any of these accounts, you need to roll it into your 401(k) before contributing to a Traditional IRA.

3. Wait once the money settles in your account

It usually takes a few days for your money to clear the bank. DO NOT buy anything within the actual account. We will do that after we are done with the conversion.

4. Call the broker to roll it into a Roth IRA

Now, you need to also have a Roth IRA account. It will be easier if both accounts (Roth and Traditional) are under the same brokerage (e.g., Vanguard, Fidelity, etc.), but it doesn’t have to be.

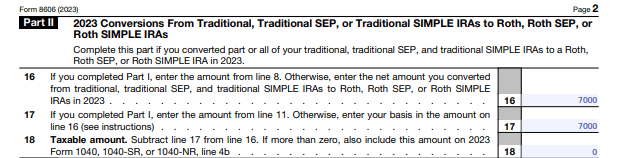

Your next step is to call your brokerage and tell them, “I deposited an after-tax amount of $X into my Traditional IRA. I want to roll it into my Roth IRA. I’m doing the Backdoor Roth.”

They will do all the work for you to convert it to the Roth IRA.

5. Invest within the Roth IRA

Now that the money is within your account, invest it. If you are curious where I invest, here is my portfolio.

Tax time

During tax time, you will receive quite a bit of paperwork. You need to make sure you classify it correctly, or if you are using a CPA, double check their work (P.S. I will tell you an easy way to fact-check it).

You will receive 3 forms from your brokerage:

→ Form 5498: This form will show you the amount contributed to the Traditional IRA.

→ Form 1099-R: This form will show the distribution from the Traditional IRA. Box 2b will be checked off.

→ Second Form 5498: This form will show you the amount you contributed to the Roth IRA.

P.S. You might receive these forms after the April 15 deadline. That’s okay, as long as you classify amounts correctly on the tax return.

With your 1040 tax return, you will need to file Form 8606. Here is an example of the completed 8606 form assuming the Roth conversion happened during the 2024 calendar year:

Now, here is how the part 2 of the 8606 form will look like:

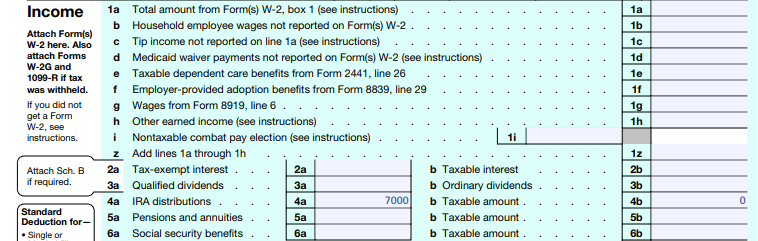

If you’ve done everything correctly (this is how you can double check your CPA) line 4b of form 1040 will be 0:

In summary, here is a simplified visual:

By the way, if you have any questions or suggestions on the type of content you want to see, just hit “Reply” to this email!

See you next Saturday!

MC, CPA