In this issue, I want to discuss selling your investments and capital gains tax.

When you sell different stocks or ETFs in your brokerage account, you generate either a gain or a loss. For example, if you buy Apple stock for $50 and sell it for $200, you generate a gain of $150.

Selling investments at a gain

- Long-term holding period

If you hold and sell your stock/ETF for more than one year, the investment classifies as a long-term holding. Long-term holding treatment is preferred over the short-term because you get preferential tax rates.

To determine how long you’ve held the stock/ETF, you generally count from the day after the day you acquired the asset up to and including the day you disposed of it.

For example, if you bought 5 shares of stock on January 1, 2024, you would begin counting on January 2, 2024. Then, on January 2, 2025, you can sell the holdings to obtain a long-term holding period.

Why is holding for more than a year important?

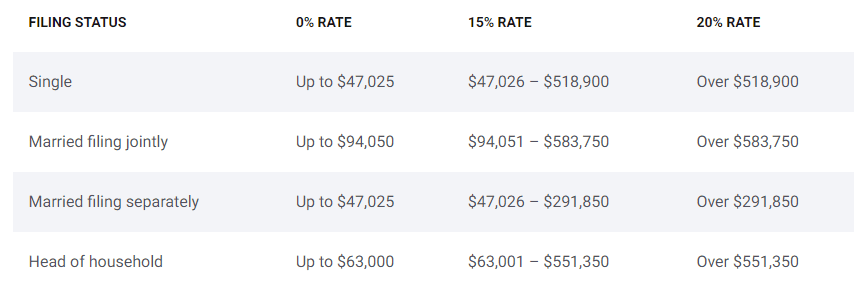

If you hold for more than a year, you get preferential treatment. Here are the tax rates:

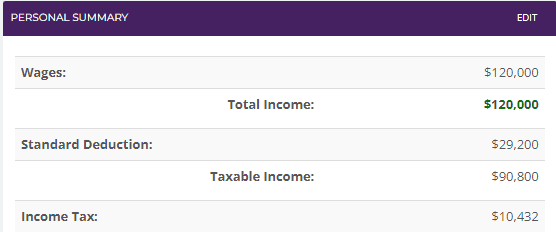

For example, if you earn $120,000 in W-2 wages and file as married, you will pay $10,432 in taxes:

Now, since the taxable income is $90,800, you can sell up to $3,250 of long term gains and still pay the same $10,432 in taxes. This due to to the 0% capital gains (up to $94,050 of taxable income):

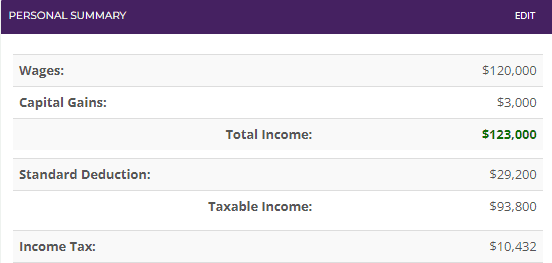

In the picture above, we can see that $3,000 of long term capital gains didn’t increase the amount of taxes paid.. Depending on your state, though, you might owe some state taxes.

- Short-term holding period

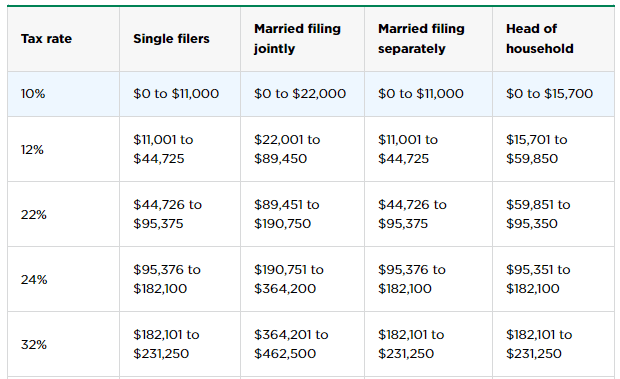

If you hold your stock/ETF for one year or less and sell it, you will pay ordinary income tax (same rate as W-2 wages):

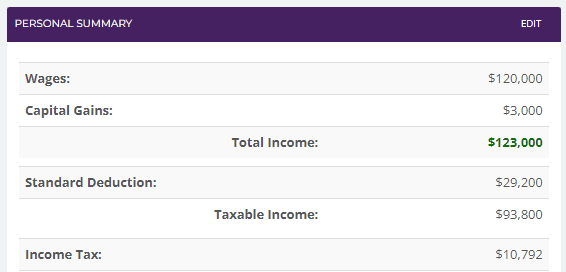

Now, let’s revisit our example where you have $120,000 in wages, but instead of $3,000 in long-term capital gains, it would be $3,000 in short-term capital gains (held for less than a year):

As you can see, we will pay $10,792 in taxes, which is $360 more than before.

So waiting a bit longer before selling just saved you $360.

Of course, there might be other reasons to sell (e.g., if the portfolio isn’t performing well, or if you need immediate access to cash), but it’s important to be aware of the tax treatment.

What if I bought the same stock/ETF at different times?

Now, you might ask, “I bought this stock on Jan 1st, then March 31st, then May 1st, what is my holding period?” The general method of calculating is First In, First Out (FIFO). This means that whenever you sell, the stocks you bought first will be used to calculate, followed by the stocks you bought after them, and so on.

You can also change the classification from FIFO to Last In, First Out (LIFO) or specific identification.

Selling investments at a loss

If you sell an investment at a loss, there is a netting process.

First, if it’s a short term capital loss, it will be applied to any short term gains.

If there is a long term capital loss, it will be applied to any long term capital gains.

If both are the same (either gain or loss), then no further action is needed.

If there is a short term loss and long term gain, they will be netted together to determine the overall gain or loss.

If you have a net capital loss for the year, up to $3,000 can be used to offset other types of income (e.g., W-2 wages, business income). The rest will be carried forward to future years.

I hope you enjoyed this one. Any questions? Reply back to this email.

MC, CPA