I started investing when I was 18 years old. I was earning ~$150/week and wasn’t able to invest much:

I didn’t have a strategy. I was just buying stocks I thought were good. No research went into it. No strategy behind allocation between retirement accounts and brokerage.

6 months ago, I simplified my investment philosophy. I created a plan that I will stick to for the next foreseeable future.

Here is how I invest now:

1. Brokerage Account:

Every paycheck, I invest around 25-35% of my income into my brokerage account.

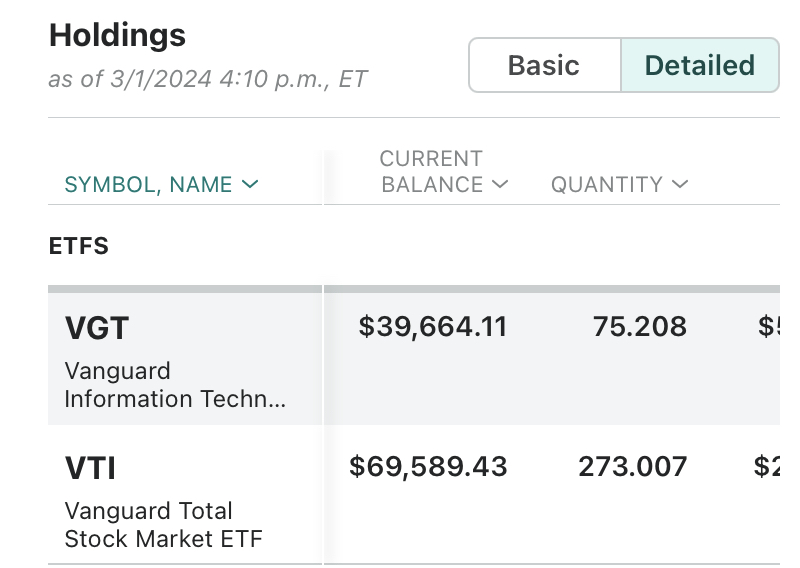

I don’t invest in individual stocks.

Instead, I buy two primary funds: the Vanguard Total Stock Market Index Fund ETF (VTI) and the Vanguard Information Technology Index Fund ETF (VGT).

VTI:

I love VTI because it tracks a variety of large, mid and small cap equity diversified across growth and values styles of investing.

It has a 0.03% expense ratio, which is extremely low, and the performance has been strong:

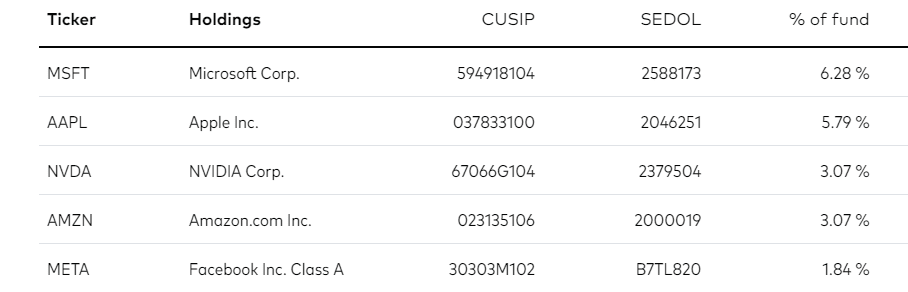

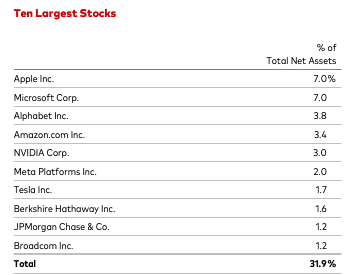

Top 5 holdings include Microsoft, Apple, Nvidia, Amazon and Facebook:

VGT

Since I’m in my 20s, I want to be more aggressive (e.g., invest in riskier funds). So, I’m currently only investing in VGT, which tracks the information technology sector.

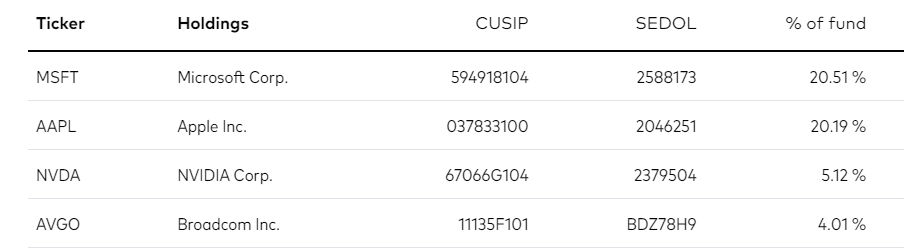

Half of the fund is invested in Microsoft, Apple, NVIDIA, and Broadcom.

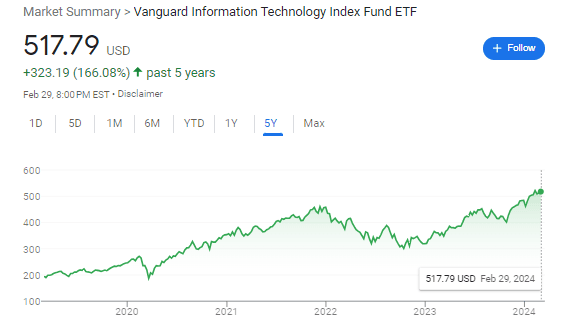

And it had a strong performance with the recent technology run:

For example, VOO (S&P 500 index) and VTI overlap by 86% in terms of weight.

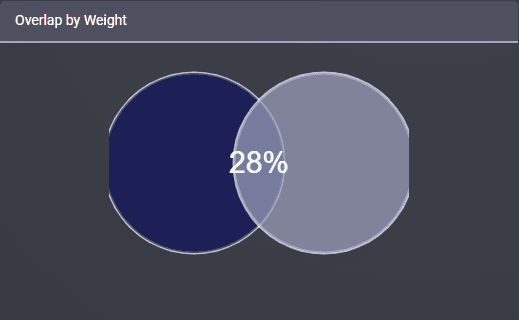

In my portfolio, VGT and VTI have only a 28% overlap.

I believe in simplicity, as it has been proven effective. The annualized performance for my brokerage account is 14%.

2. 401k

I recently increased my 401k contribution from 5% to 15% per paycheck. I also receive a 100% match up to the first 5%. I’m in the 24% tax bracket, so every dollar extra I invest in the 401k receives a 24% tax deduction.

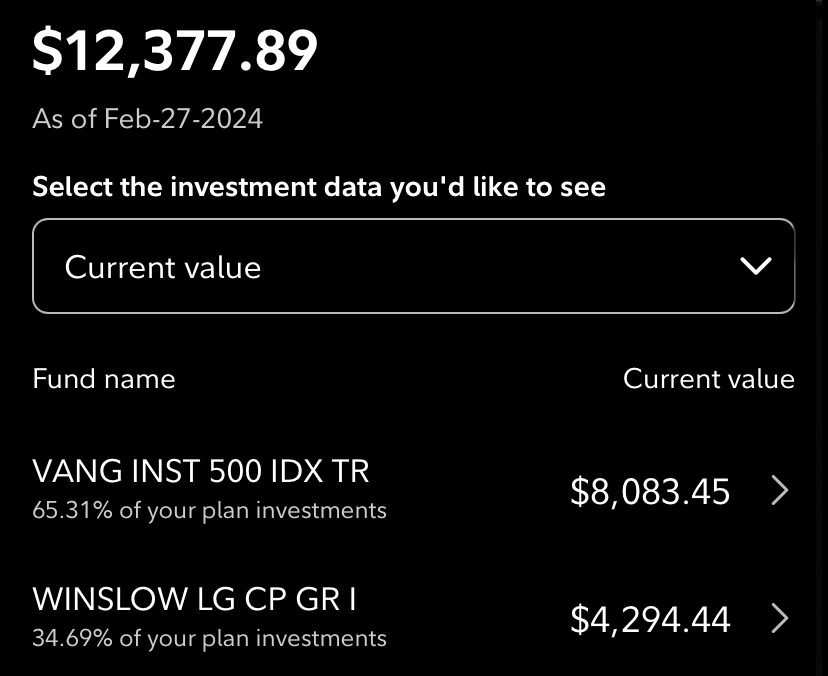

Within my 401k, I primarily invest in one fund – Vanguard Institutional 500 Index Trust. It tracks the performance of the largest 500 companies in the US.

I love this fund because it has an extremely low expense ratio. Originally, I invested a little in the Winslow Large Cap Growth Fund, but the performance isn’t that good. Also, it has a high expense ratio (0.71%). So I changed 100% to the Vanguard fund.

The total annualized return is 12.09%.

I highly suggest reviewing your 401k allocations and selecting good funds (like S&P 500) with low expense ratios.

I will also be able to withdraw from 401k a lot earlier than 59 ½ due to 72(t) or Rule of 55, so I’m not worried about liquidity.

3. Roth IRA

Roth IRA is extremely powerful as it allows you to withdraw your money tax-free during retirement, doesn’t require RMD, doesn’t count toward Medicare premiums, and lowers social security taxation.

100% of my money within the Roth IRA is invested in the Vanguard Total Stock Market Index Fund ETF (VTI).

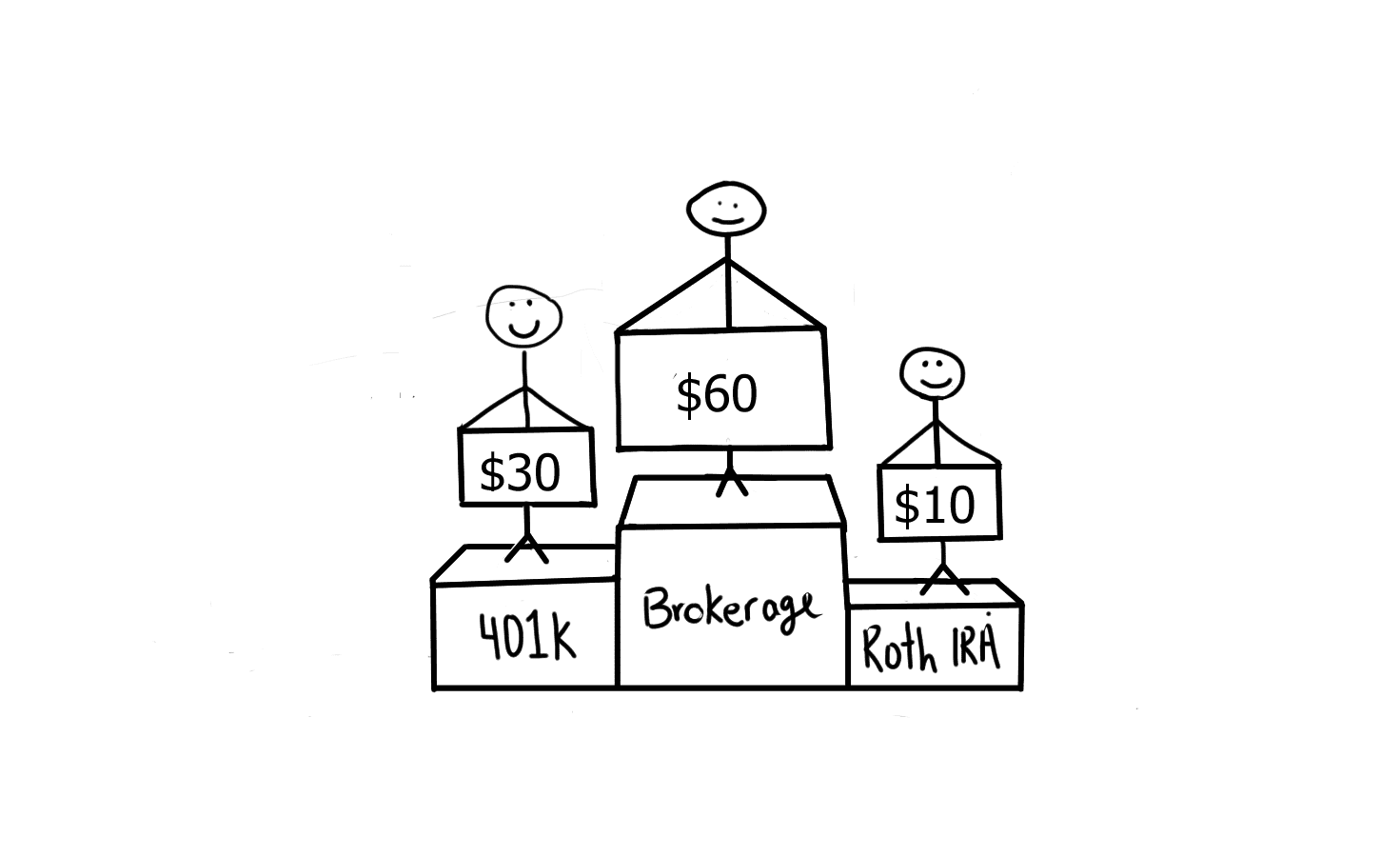

So overall, here is how the allocation looks for every $100 of my investments:

Regardless of your investment strategy, just stay consistent and think long term.

See you next Saturday.