Inflation has been sticky.

The Consumer Price Index (CPI) rose 2.7% over the year in November, up from 2.6% in October, marking the second consecutive month that inflation has increased.

Many people are familiar with I-bonds. If you aren’t, check out my previous newsletter. Today, however, I want to focus on another great way to safeguard against inflation: Treasury Inflation-Protected Securities (TIPS)

What Are TIPS?

TIPS are bonds issued by the U.S. Treasury that provide protection against inflation. The principal and interest payments of TIPS are adjusted daily based on the changes in the Consumer Price Index Urban Consumers (CPI-U).

If there is inflation, the value of your bond grows, and if there is deflation, it falls.

A TIPS fund pays interest twice a year. How do you calculate the interest? If a TIPS fund has an interest rate of 2% and the index ratio is 1.030 on the date of payment, a $1,000 bond will pay:

$1,000 * 1.030 * 2% / 2 = $10.30.

Where to use TIPS?

TIPS are bonds.

The main role of TIPS bonds in a portfolio is similar to other bonds — they provide good diversification of equity risk, since inflation typically has a negative correlation with equities.

Now, if you are young, bonds are generally not recommended, and TIPS wouldn’t be needed.

If you are closer to retirement, bonds are great for reducing your risk, and TIPS bonds should be evaluated against other bond types.

How to get TIPS?

- At Auction

You can purchase directly from the U.S. Treasury (via TreasuryDirect). TIPS have different maturities (5,10,30 years). When TIPS mature, you receive either the adjusted principal or the original principal, whichever is greater.

- Secondary Market

You can buy them through brokerage accounts (Vanguard/Fidelity)

- ETFs

There are TIPS ETFs. For example, Vanguard offers the Short-Term Inflation-Protected Securities ETF (VTIP). One thing to keep in mind with ETFs is that they buy and sell TIPS constantly, so you are exposed to duration risk.

VTIP buys and sells TIPS constantly; therefore, you will always have duration risk no matter how long you hold it.

However, if you buy a 10-year TIP at auction, your duration risk will decrease year after year, and at maturity, you will get your principal back plus potential adjustments.

Performance

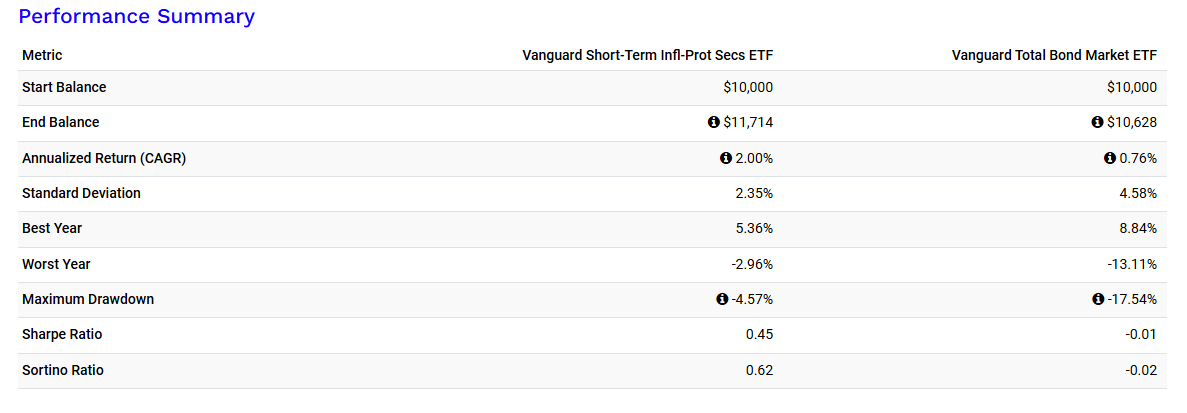

So, how would a TIPS ETF perform compared to other bond products?

If we look at BND, the Vanguard Total Bond Market Index Fund ETF, versus VTIP over the last 10 years, we can see that VTIP outperformed:

Taxes

The biggest issue with TIPS is that they are tax-inefficient. Both the inflation adjustment to the principal and the interest payments are taxable. However, they are exempt from state and local taxes.

If you want to hold TIPS in a taxable account, you might want to consider I-bonds instead, since the tax deferral is likely to be worth more than the yield difference. However, TIPS are more marketable than I-bonds because they can be bought and sold on secondary markets.

If you hold TIPS through an ETF in a taxable account, the ETF will distribute the taxable income to you as dividends. Tax reporting is similar to other Treasury bond funds.

Tip: TIPS are effective in tax-advantaged accounts like IRAs, since the taxation issue doesn’t apply.

Overall, TIPS can be great to safeguard against inflation or diversify a bond portfolio. Otherwise, for cash-like holdings, Money Market Funds or HYSAs are still preferred due to their stability.