Most of you are familiar with the basics of a 401(k) plan, but there are still many nuances that many aren’t aware of (hardship withdrawals, after-tax account, etc).

So, let’s dive into everything you need to know about a 401(k) plan.

First, it’s an employer-sponsored retirement plan. If your employer doesn’t offer one, you can’t contribute or enroll. You should contact your HR if you aren’t sure.

Types of 401(k)

Employers typically offer two main types of 401(k):

1. Traditional 401(k)

When you contribute to a pre-tax account, you receive an immediate tax deduction. The tax gets deferred (postponed) until you start withdrawing money at retirement age.

For example, if you make $100,000, you will pay $13,841 in federal taxes. If you contribute $5,000 to a pre-tax 401(k), you will pay $12,741 in federal taxes. So, the $5,000 contribution reduced your taxes by $1,100.

2. Roth 401(k)

With a Roth account, you don’t get an immediate tax deduction; however, you pay no taxes on withdrawals at retirement age.

In our example, you will still pay the same $13,841 in federal taxes, but your contributions grow tax-free.

Which account should you contribute to? Generally, it comes down to the decision of marginal tax rate now vs. in the future. I wrote more about this decision in another newsletter.

3. After-tax 401(k)

Some employers might also offer an after-tax 401(k). This account is also part of the strategy called a “Mega Backdoor Roth.” I wrote more in-depth about it here, but if you are just starting out, don’t worry too much about this one.

Match

The big benefit of contributing to a 401(k) account is that many employers offer a match to incentivize savings and retain employees.

For example, they might say, “We provide a 100% match on up to 5% of your salary deferral.” In this case, if you contribute 5% of your salary, you will receive another 5% from your employer (or a 100% return on your money). This is exactly why the first step in building your financial stability is to contribute at least up to the match.

Vesting rule

One thing you need to keep in mind is vesting rules. In simple terms, this means the timeframe for how long you need to stay with your company for the match amount to be yours.

Many employers have a 3-year rule with 33% vested every year. So, if you quit after year 1, you will keep only 33% of your employer contributions. If you stay for at least 3 years, you will keep it all.

Importantly, you always keep your own contributions.

Contribution Limits

The total employee contribution limit for 2024 is $23,000 (traditional or Roth).

If you are age 50 or over, you are eligible for an additional catch-up contribution of $7,500.

Investment options

You are limited to the investment options that your employer provides. Some employers have amazing options, others not so much.

Target funds

Most employers offer target funds as an investment option. These are funds that have “target retirement year” in their name:

I personally believe they are too conservative (too much bond allocation), and some might have a high expense ratio, but they are better than nothing. If your employer has automatic enrollment in a 401(k), they will typically allocate your money to these funds.

Aside from target funds, you can also select other funds. I personally like the Vanguard S&P 500 fund and am 100% invested in that fund. My wife doesn’t have a Vanguard fund but has Fidelity’s S&P 500 and is 100% invested in that fund.

Vanguard and Fidelity are great funds as they have low fees.

Withdrawals

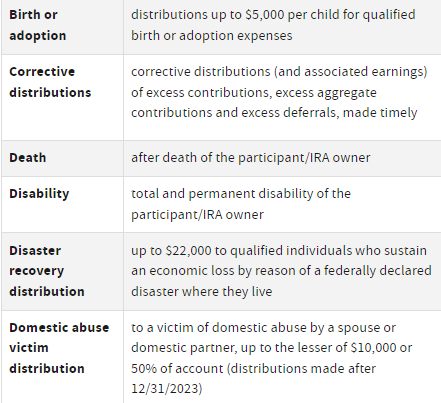

Withdrawals from your 401(k) plan before age 59½ will come with a 10% penalty unless you meet an exception:

When you separate from your employer, you can keep the plan with them or roll it over to an IRA account.

There are two decent strategies that can help withdraw from a 401(k) early (specifically for people looking to FIRE):

Both of these help avoid the 10% penalty.

Taxes

Whenever you withdraw from a traditional 401(k) plan, you will be subject to taxes on your withdrawal.

Loans

If you plan to withdraw before age 59½ due to hardships, taking a loan is often a better choice. It helps you avoid the tax and penalty.

Depending on what your employer’s plan allows, you could take out as much as 50% of your vested account balance or $50,000, whichever is less. An exception to this limit is if 50% of the vested account balance is less than $10,000; in such a case, you may borrow up to $10,000.

Remember, you’ll have to pay that borrowed money back, plus interest, within 5 years of taking your loan in most cases. If you separate from that employer, you will have to pay it all back. The nice thing about a 401(k) loan is that the interest is being paid to your own account.